Built on Infrastructure

Powered Land

June 29, 2026 4 Minute Read Time

Overview

U.S. electricity demand is entering its strongest four-year expansion since 2007, marking the most aggressive growth phase since the turn of the century. Total consumption is now forecast to add 420 billion kWh, pushing total demand toward 4,800 billion kWh by 2030, according to the International Energy Agency (IEA). Data center expansion is the primary catalyst, accounting for roughly half of all new load and projected to consume nearly 10% of the entire U.S. grid by the end of the decade. This power concentration will surpass the combined energy footprint of the aluminum, steel, cement and chemicals industries.

Following Q1 2026 earnings guidance, the “big five” listed hyperscalers—Amazon, Alphabet, Microsoft, Meta and Oracle—have raised guidance, with a combined capex for 2026 now tracking $740 billion–$760 billion, marking more than $1.6 trillion since 2023. The proportion earmarked for data center facilities and power infrastructure remains high. In its recent Q1 earnings call, Alphabet confirmed approximately 40% of its capex budget is dedicated to data centers and networking equipment.

However, power assets and related grid infrastructure take significantly longer to build (and connect) than data centers. The divergence between compute deployment and grid expansion has become a critical bottleneck in 2026. Hyperscale data center campuses take 1–3 years from planning to commissioning, compared to 5–15 years to build the transmission upgrades, substations and transformer capacity required to supply them, according to the IEA. This mismatch resulted in the first contraction of the U.S. data centers construction pipeline in five years, with capacity under development falling 5.6% to 5,994.4 MW by the end of 2025. Secondary headwinds include permitting, zoning and power procurement hurdles, as concerns over aging grids also grow.

These constraints are accelerating the repricing of powered land, where “speed-to-power” now sits alongside location as a primary determinant of land value. Sites designated as “Powered Land” are now valued as critical hybrid assets, with premiums driven by pre-secured interconnection agreements and real estate optionality.

The power-demand regime shift

Data centers require near-continuous high load factors compared with traditional industrial demand, which usually involves intermittent demand peaks. Newer AI facilities also require significantly higher power densities—exceeding 120 kW per rack—as well as advanced liquid-cooling systems that place further pressure on local distribution infrastructure. As AI compute demand accelerates faster than power generation, transmission and digital infrastructure can keep pace, access to power becomes the key determinant of data center growth and geographic distribution. Regional differences in power availability, interconnection timelines, and grid readiness now often supersede traditional metrics such as land costs, location, labor and tax incentives. By 2030, about one in five data center campuses is expected to exceed the gigawatt scale, increasing to one in three by 2035, with power delivery as the primary constraint.

The complex process to secure power is mediated by region, project size and regulatory channel. For large-scale projects in high congestion regions, such as California and the Mid-Atlantic states, interconnection queues were six years in 2024, independent data analyzed by Lawrence Berkeley National Laboratory (LBNL) shows. However, time can stretch up to 15 years at the extreme after interconnection queues and construction time is factored in.

Development vs. Grid Infrastructure Timelines: the mismatch between asset development and power delivery creates a structural scarcity premium for powered land

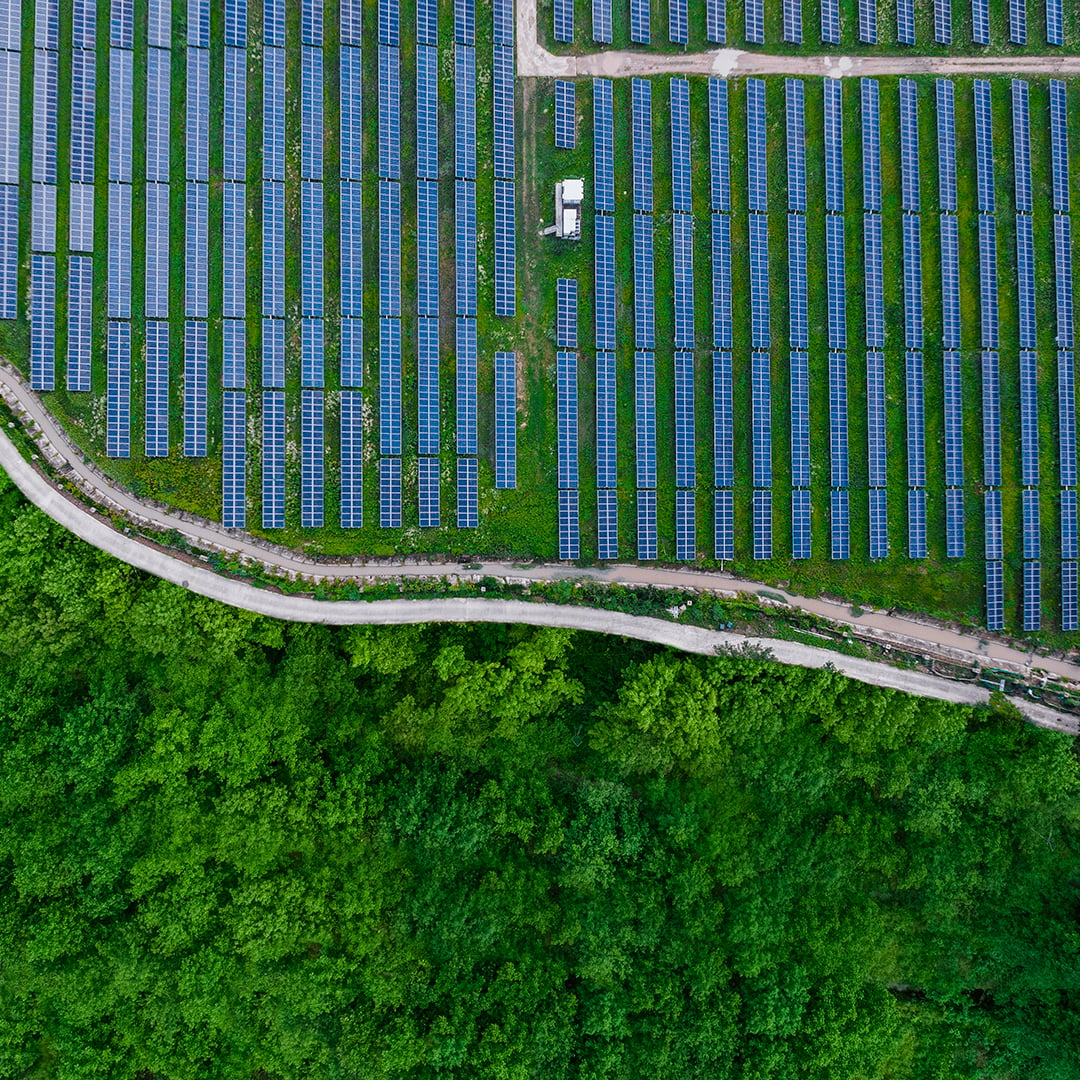

Renewables renaissance

The U.S. energy complex remains dominated by natural gas, nuclear and coal, which together account for 75% of 2025 domestic electricity generation. From 2026 onwards, solar and wind combined will become the second-largest source of U.S. electricity. Over the next two years, solar and wind will drive net growth—rising from 16% in 2024 to 21% by 2027, according to EIA projections behind natural gas while ahead of coal and nuclear. Within this mix, solar is the primary catalyst, nearly doubling its share from 5%–9% over the forecast period.

Renewables benefit from faster speed-to-market, lower installation costs and insulation from fossil-fuel price volatility. Therefore, integrating solar, storage and hybrid generation is an effective way to shorten time-to-power timelines, although transmission and storage lags arguably limit renewables’ ability to resolve near-term market-level supply constraints unless deployed as onsite, behind-the-meter (BTM) solutions.

U.S. Electricity Generation (%) Mix: solar and wind combined will become the second-largest source of U.S. electricity, surpassing nuclear for the first time

Energy market volatility further reinforces the strategic value of power security. The conflict in Iran and disruption to Strait of Hormuz shipments have sent oil and natural gas prices sharply higher, with geopolitical risk directly translating into higher data center operating expenditure. This risk upgrades the investment case for renewables and diversified storage from optional to critical. Sites capable of hosting onsite generation carry an energy premium for their insulation against global energy market swings.

Where real estate becomes infrastructure

Viable powered-land sites incorporate scalable onsite generation, battery storage and operational systems that allow facilities to run either in parallel with or independently from the grid. In this context, powered land is real estate that functions as an enabling layer of critical infrastructure. Value is shifting upstream from buildings (the real estate) to system access—power, interconnection and permits (the infrastructure).

The reliable power delivery premium is visible in market fundamentals. Primary market vacancy hit a record-low 1.4% in 2025 while operators pass through power scarcity to occupiers in multi-tenant data center facilities via higher wholesale colocation pricing, despite slower supply growth. This power delivery premium extends to capital markets, as BlackRock’s Global Infrastructure Partners and EQT acquisition of AES Corporation in March shows. The major U.S. power generation and energy infrastructure company was acquired for an enterprise value of $33.4 billion, a 40% premium. Developer-operators that compress multi-year interconnection and permitting timelines can monetize the premium associated with reliable power delivery. Hyperscalers now make leasing decisions based on who can secure and deliver power on a predictable timeline.

Underwriting powered land

The deal economics of powered land involve applying infrastructure-style underwriting discipline to real estate development. Three interrelated variables are the focus: power deliverability, development execution and long-term commercial durability.

Power deliverability

Interconnection rights, grid access and development approvals are the primary determinants of site viability. Access to substations, transmission networks and available capacity within regional grids determines whether electricity can be delivered within feasible development timelines.

Regulatory structures are now a formal component of the underwriting equation. The Ratepayer Protection Pledge (RPP) federal mandate, enacted in March 2026, established a federal energy self-sufficiency framework for large-scale data center development. Under the pledge, operators are expected to fund required network upgrades, secure additional power capacity and shield residential consumers from electricity price increases associated with large industrial loads. At the state level, jurisdictions including Texas, Minnesota and Oregon have further integrated these principles into permitting processes, including requirements around upgrade funding, curtailment and independent generation during grid emergencies. Utility commitments and credible “speed-to-power” pathways are therefore critical. Binding energy service agreements that guarantee delivery timelines and commit the utility to build before vertical development are often required.

Development execution

Development execution risk can materially affect project viability even where electricity is available. Operators’ capability has risen in prominence as an underwriting variable. For example, the ability to manage constraints (e.g., labor markets, supply chains, construction costs and equipment availability) all impact project schedules. At the same time, construction complexity is increasing, and developments are bifurcating into “powered shell” facilities (where electricity capacity is secured prior to tenant fit-out) and “turnkey” facilities (delivered ready for immediate occupancy).

Hyperscalers increasingly require significantly higher rack densities—routinely exceeding 120 kW per rack—which demand greater engineering expertise to install higher-voltage distribution architectures. In shared facilities, AI and cloud workloads co-exist within the same assets with varying hybrid cooling, power and density requirements. Liquid cooling, which helps maintain performance of AI systems at scale, can require significant upgrades of local water and power distribution infrastructure. These trends favor developers with scale and established procurement relationships.

Commercial durability

The project economics of powered land rely on data quality, underwriting standards and governance frameworks that oversee the integrity of processes and decision-making. AI-enabled analytics can improve forecasting and scenario modeling by identifying patterns in large datasets, thereby enhancing audited decision-making. However, where governance controls are weak or underlying assumptions are inaccurate, errors may cascade into schedule slippage, cost overruns and impaired returns.

Powered Land: Risk Matrix: risk categories, early warning indicators and mitigation strategies

Conclusion

Powered land reprices real estate based on power deliverability. Extrapolating capacity forecasts to meet forward data center electricity demand implies tens of gigawatts of additional generation capacity and thousands of acres of powered land across the U.S. over the remainder of the decade.

The opportunity set is therefore long duration, but outcomes will be uneven. A plethora of variables can materially shift project economics—from regulatory reversals, to state-level changes to how network upgrade cost liabilities are assigned, as well as hyperscaler demand fluctuations and community opposition to AI data centers in residential-adjacent markets. Consequently, operator selectivity is vital. Not every powered site will deliver long-duration cash flows, and outperformance will depend on site-level due diligence, credible power pathways and scenario-tested underwriting.

2 Wood Mackenzie Q2 2025 transformer survey; large power transformers averaging 128 weeks, GSUs 144 weeks (Power Magazine, Jan 2026).

3 High-capacity unit lead times averaging 90–128 weeks vs pre-pandemic norm of ~40 weeks (Data Center Economist, Nov 2025; Latitude Media, Feb 2026).

4 Lawrence Berkeley National Laboratory, 'Queued Up' 2024; FERC interconnection queue data.

5 IEA, 'Data Centre Electricity Use Surged in 2025,' April 2026. Figures represent conditional offtake agreements; commercial operation not expected before early 2030s.