Why Core Real Estate?

The Case for Global Core

October 9, 2023 15 Minute Read Time

Introduction

Institutional investors allocate an average of 10% of their portfolios to real estate, an asset class that offers attractive risk-adjusted returns, high and stable income, the potential to add value through active asset management, at least partial inflation protection and portfolio diversification. It’s possible to enhance these benefits further by investing globally.The benefits of investing in overseas, as well as domestic, real estate markets are centered around three pillars. Firstly, global Core/Core+ real estate strategies enable investors to capture higher risk-adjusted returns and potentially secure a higher level of inflation protection. Secondly, going global provides added diversification and liquidity benefits which reduce risk without sacrificing return. Thirdly, global Core/Core+ strategies allow investors to capitalize on regional differences in real estate markets across Asia, the Americas and Europe, potentially delivering exposure to real estate subsectors that may not be available domestically as well as access to more liquid markets.

Yet, despite the benefits of global Core/Core+ strategies, the vast majority of investors across all regions have historically had a bias toward domestic markets. This is due to familiarity, costs and taxation; all of which can be overcome by deploying solutions ranging from private and public funds to holding and managing direct assets via global platform providers.

If these solutions are executed properly, investing globally can enhance returns and reduce risk in today’s uncertain macroenvironment, particularly when regions are at different stages of inflation management and market cycles. Significant repricing in certain global real estate markets has opened up opportunities to acquire high-quality assets at attractive prices. The result is the opportunity multiplier effect of going global.

What real estate has to offer

Institutional investors have steadily increased their allocations to real estate in recent years. Today, real estate is the third largest asset class after equities and bonds.Institutional investors allocate on average c. 10% of their portfolios to real estate

Annualized Global Total Returns and Volatility for Asset Classes (2001 – 2022)

- Over the long run, direct real estate’s strong and stable income returns have outperformed other major asset classes

- Over the last 45 years, U.S. real estate fund returns have been in negative territory on only five occasions and even then, the stable income generated has generally outpaced any negative movement

It's not all about income

Real estate offers the opportunity for active managers to add value through asset management initiatives. Refurbishment, renovation, redevelopment, reconfiguration, and repositioning are strategies that can be deployed to increase a property’s sustainability credentials, ensure the property is tech-enabled and deliver the amenities employers and employees seek. By accommodating the needs of occupiers, properties can be leased at higher rents, vacancy rates can be reduced, higher-quality cash flows can be generated, leading to an increase in value.Asset managers can also add value by securing more competitive financing that enhances the economics of the property or carrying out research that uncovers future improvements to infrastructure in the surrounding area. Multiple touch points exist for active managers to add basis point(s) of outperformance in various areas which together add up to meaningful value.

And then there’s risk reduction

The graphic below shows that real estate has a low correlation to other asset classes:

Global correlation of NOI growth and return with inflation using annual figures, 1983 – 2022 (past 40 years)

What global real estate has to offer…

The benefits of investing in global Core/Core+ real estate strategies are centered around three pillars:- Return enhancement: the addition of a stable source of income and some inflation protection can be accretive to portfolios

- Risk mitigation: the greater diversification and liquidity benefits offered can decrease risk without giving up return

- Opportunity multiplier effect: the regional differences seen across global real estate markets magnifies the opportunity set

Pillar one: return enhancement

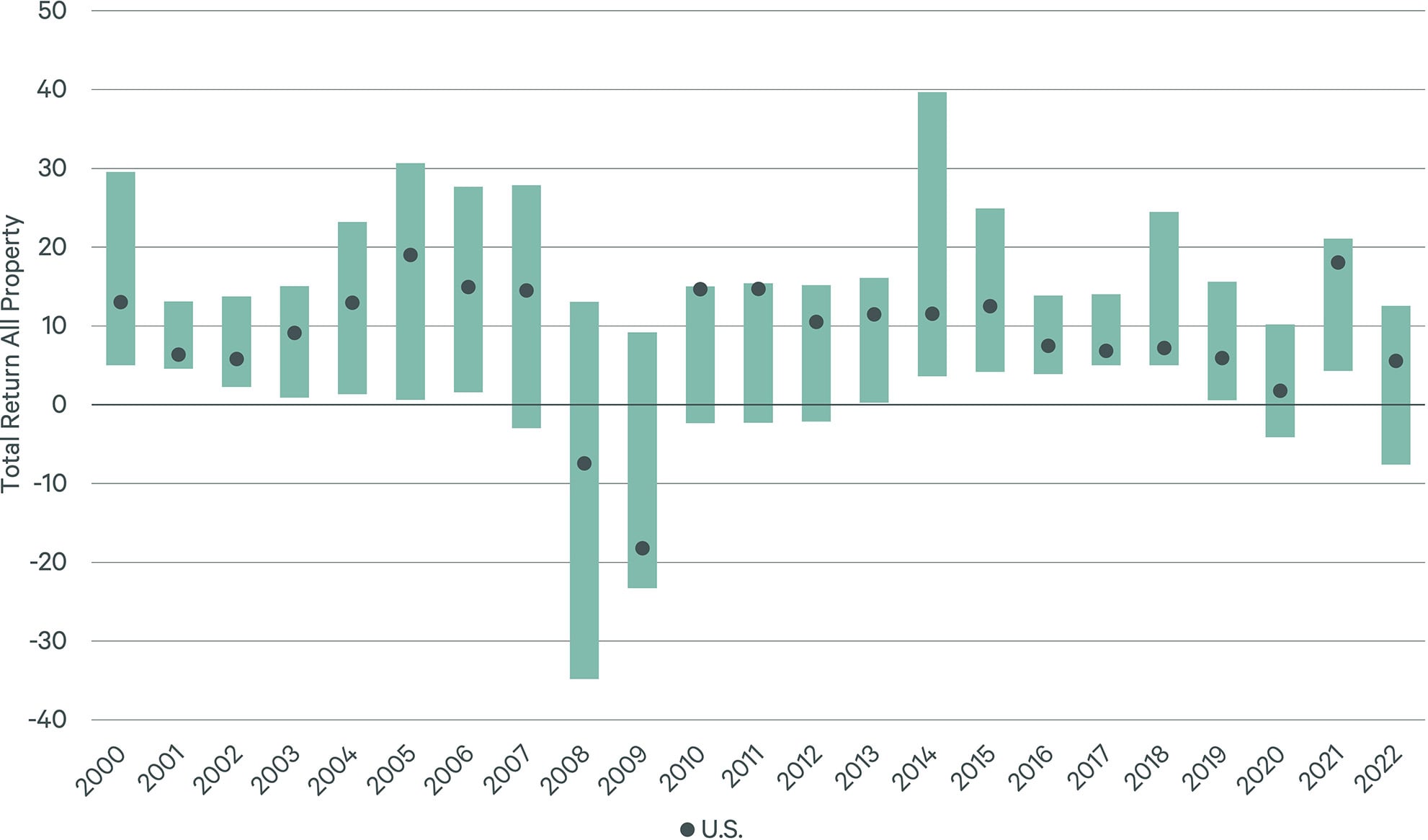

As the graphic below highlights, U.S. real estate total returns exhibited a high degree of cyclicality over the last 20-year period: between 2010—2013, U.S. real estate total returns outperformed; between 2014—2020, they underperformed:Range in global real estate total returns by country, per annum, local currency

Targeted market selection can capture enhanced returns.

Leverage can increase returns too, but the cost of debt impacts the returns achieved. Securing competitive terms helps maximize the benefits of leverage. And yet, as the graphic below illustrates, the best debt terms can be found in different markets at different points in time and stages in the cycle. Investing globally provides greater potential for more attractive financing.Spread between Total Returns and Corporate Borrowing Rates (period average)

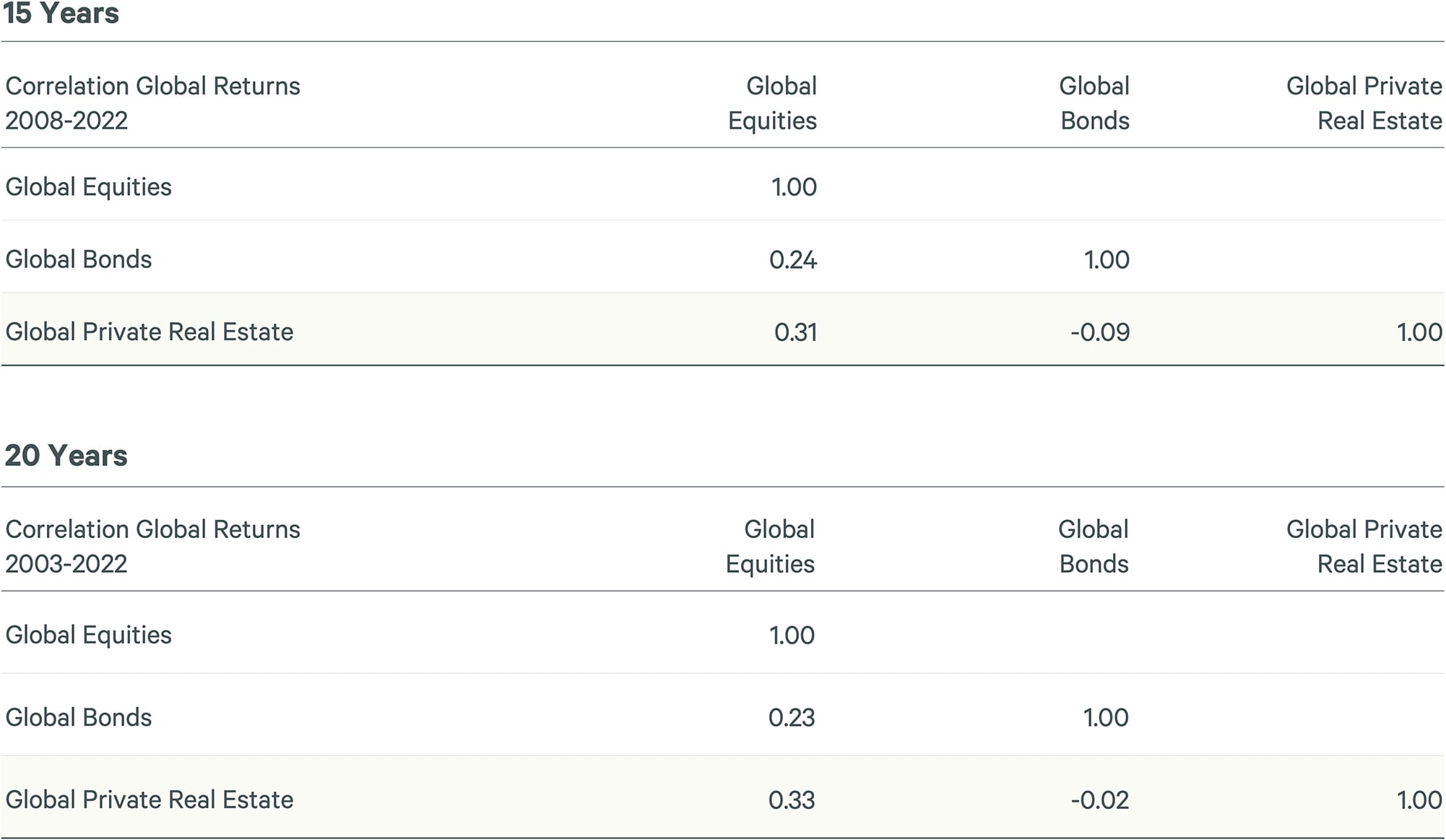

Pillar two: risk mitigation

Global real estate markets are at different stages of the economic cycle and tend not to be fully synchronized:Total Returns by country, % in local currency

Real Estate Market Total Return Correlations* 2006 – 2022, local currency

The benefits of diversification are at work at the city level too. Cities within the same country tend to be highly correlated with each other. CBRE IM looked at 22 cities in the U.S. and found that the average correlation between them was 0.87. When compared with 65 non-U.S. cities, the average correlation fell to 0.50.

Effect of international diversification is substantially larger than of domestic diversification.

Correlation coefficients between returns of 87 key cities globally

RCA long-term average liquidity scores — Q1 2008 – Q1 2023

Pillar three: the opportunity multiplier effect

Investing in global Core/Core+ real estate strategies opens up a wider set of investment opportunities. Put simply, it provides more options for investors, even for those in North America, the largest institutional investment market globally. Investors are able to gain exposure to faster-growing markets and subsectors.

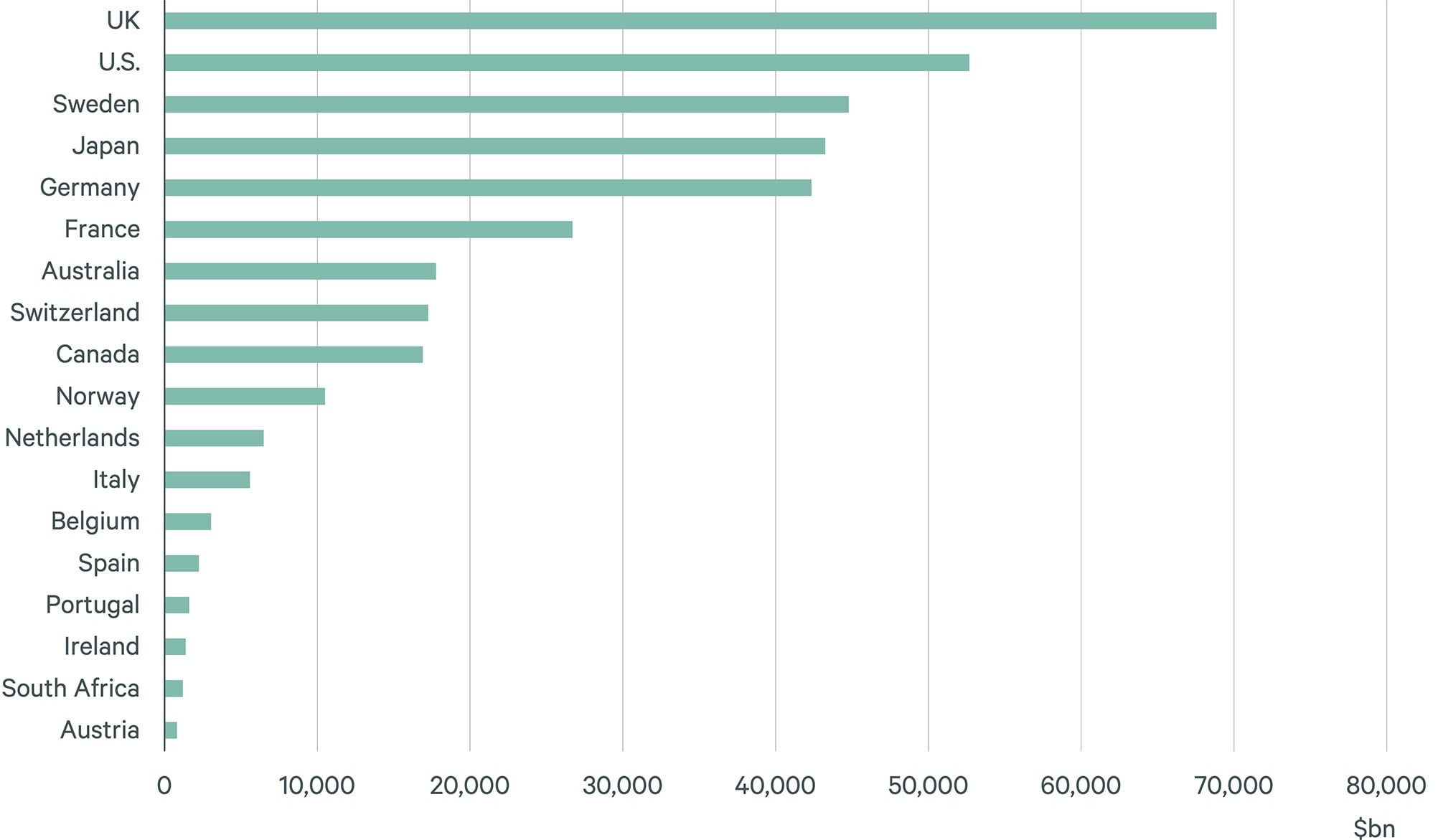

It also provides a wider set of investment opportunities in terms of increased exposure to more niche or emerging growth sectors. The graph below highlights the size of niche markets at the country level:

Estimated size of niche sectors

Ratios of return over standard deviation for sectors, 2008 - 2022

Domestic bias

Despite the benefits of going global, institutional real estate allocations have a strong bias to their domestic regions.Current real estate allocations to an investor’s domestic region, % total real estate

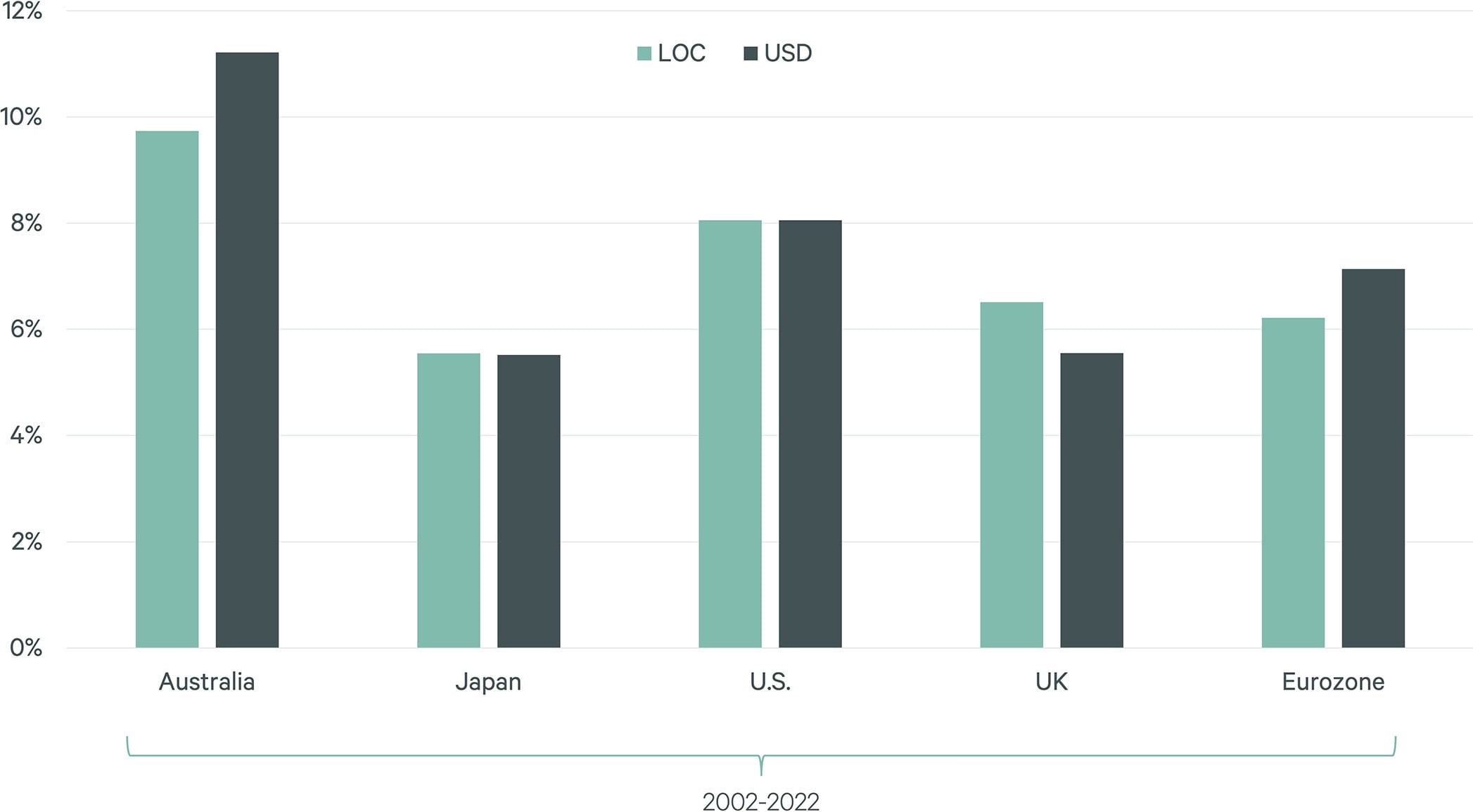

The graphic below showing 2022 real estate returns in local currency and USD and appears to validate investor concerns over the effect currency movements have on returns:

The currency effect perhaps not as strong as feared and can be mitigated.

Each country has its own tax regime. Investing in global real estate may, therefore, create greater complexity. Tax risk, however, can be mitigated by expert tax advisors via the use of tax-efficient and legal structures. Taxes can be minimized through sound legal advice and execution.The tax factor doesn’t have to be concerning

Other factors are at play too, such as reduced liability matching, whereby exposure to foreign interest rates and inflation reduces real estate’s role in liability-driven investment programs. Certain real estate markets benefit from a more explicit linkage between inflation and leases than others (e.g., Europe has annual rent indexation). Sound portfolio management and planning can overcome such issues.The solution: a global platform

The key to accessing global investment opportunities is the utilization of a global platform that has scale and reach, boots on the ground and deep local knowledge. Regulatory, tax and cost landscapes can be navigated effectively and opportunities to add value through asset management and/or development can be sourced and capitalized on. Ideally, a global platform will offer a full suite of solutions so that investors can select the right one for their own needs:- Private Direct: investing directly in overseas real estate markets

- Private Indirect: investing in commingled funds, joint ventures, programmatic ventures that provide investors with an alternative to investing directly in overseas markets. All involve partnering with specialist local operators.

- Public: publicly traded funds such as REITs that invest in global and/or regional real estate markets.

The graphic below highlights what each investment format has to offer:

Optimal investment format composition depends on a range of investor specific goals

Why invest in global real estate now?

Investing globally brings greater diversification that can help reduce risk while also capturing higher returns in today’s challenging macro environment. A U.S. investor can increase exposure to inflation-linked rents by investing in Europe where these are more prevalent. A European investor can gain exposure to niche but fast-growing areas of real estate, such as self-storage, by investing in the U.S. where the sector is more established compared to other parts of the world.An opportunity exists now, however, to acquire prime assets at a lower cost basis. That’s because many global real estate markets have undergone significant repricing. And as the graphic below shows, some parts of the world have repriced quicker than others:

The case for investing in global real estate has never been stronger.