Market Research

Quality and Modernity Deliver for U.S. Logistics

March 25, 2024 15 Minute Read Time

Introduction

The U.S. logistics market has broadly normalized after extraordinary conditions during the Covid-19 pandemic. The aftereffects on the U.S. logistics sector, however, have likely just begun to play out. The combination of higher e-commerce penetration, ongoing disruptions to supply chains, higher interest rates and shortages of workers have brought about a new normal in logistics operations that we believe will be defined by the following trends:

- Adoption of new technologies to enhance speed, accuracy and overall efficiency of supply chain operations requiring modern design features and specifications.

- Supply chain resiliency measures focused on diversifying material sourcing and heightened management of strategic inventory levels across geographic networks.

- Increased integration of online and in-store sales channels.

- Lower levels of supply of modern logistics facilities.

- Cap rate compression as interest rates moderate.

- Changing demographics and customer habits around using e-commerce.

We believe these trends support investment into U.S. logistics real estate—but not just any logistics real estate. The new technologies on which contemporary occupiers depend, like robotic retrieval, automated sorting and stacking, EV fleets, and high-throughput circulation, require a set of design features and specifications only found in newly-built modern facilities.

In this paper, we explore how these trends shape our investment thesis for U.S. logistics and present the reasons why we expect modern logistics real estate to deliver the highest total returns of any sector in the years to come.

Logistics operators are investing in technology

In response to the disruptions to supply chains during and since the pandemic, logistics firms are significantly increasing their investment into technological solutions. Per the Materials Handling Institute’s (MHI) 2023 survey, 90% of respondents expect to spend at least $1 million on digital supply chain technologies, up from just 50% prior to the pandemic.

Figure 1: Planned investment in supply chain innovations

Many of these technologies are already well-established at large logistics operations. Amazon depends on 750,000 mobile robots to fulfill orders and is the largest manufacturer of industrial robots in the world. Large modern fulfillment centers use as much as 60 miles of conveyor belts. Wearable tech and automated sensors support the flow of goods and direct human workers.

The effectiveness of these technologies, however, ultimately depends on the software conducting their operation. Respondents to the MHI survey cite AI as having the greatest potential to disrupt the industry, while advanced predictive analytics offer the largest potential competitive advantage.

New technologies require next-generation logistics facilities

New technologies require physical logistics spaces that provide key building features. The following building features were rated as the most important in CBRE’s 2022 U.S. Industrial & Logistics Occupier Survey:

Figure 2: Importance of logistics building features

- Clear Height: Clear heights ranked as the single most important consideration in CBRE’s 2022 occupier survey. Occupiers are now looking for clear heights of 36-40 feet compared to 18-32 feet in older buildings. New technologies can make use of the higher clear heights and since occupiers pay rent per linear square footage, larger building volumes create efficiencies.

- Floors: Higher clear heights mean more weight per square foot and thus require heavier foundations. The new normal of at least 7”+ reinforced slabs replaces the 4” standard and supports enhanced structural roof upgrades and the load carry capacity required for conveyance/material handling systems. Additionally, robotic automation systems require super flat, seamless, and durable floors.

- Roof load: Roof loads above 15 lbs. per square foot are the new standard, up from 9-10 lbs. per square foot. The higher roof loads support heavy mechanical systems, HVAC, solar panels, and potentially even parking on rooftops.

- Column Spacing: Support columns can impede efficient goods storage and movement. Fewer columns increase flexibility both on the warehouse floor and speed bays. Modern logistics properties have at least 50 feet between columns, compared with 40-45 feet in older properties—resulting in about 30% fewer support columns.

- Truck court depth and leading bays: Large modern logistics facilities have 30% more land area than similarly sized legacy product, allowing for larger truck courts with maneuvering areas, trailer parking for onsite storage and ample car parking. A truck court depth of 130 feet or more facilitates quicker loading and unloading and better maneuverability for truck fleets. Larger land areas also provide space for future expansion.

- Enhanced Power: Modern logistics facilities must provide sufficient power to operate the conveyor belts, truck carousels, EV charging, battery storage capacity, internet connectivity and computer operations on which logistics operations now depend. Reliable, secure and cost-effective power supplies include rooftop solar panels, enhanced electrical conduit throughout the truck court, closed-loop battery storage onsite and EV charging stations. Buildings with renewable energy sources onsite, such as rooftop solar panels, provide a more sustainable solution—a rooftop installation can power up to 80% of a facility’s energy use.

- Enhanced utilities: Larger and taller buildings require adequate water pressure to support modern fire suppression systems. Additionally, energy-efficient buildings not only generate cost savings for businesses, but also help meet sustainability requirements.

- Amenities: Talent procurement and retention for warehouse occupiers has become critically important over the last few years as U.S. warehouse employment grew by over 58% from January 2018 to January 2022. Amenities such as gyms, showers and outdoor space help attract and retain employees and reduce staff absences.

Supply chain resiliency creates logistics demand

The pandemic, weather volatility, geopolitics and other factors have all disrupted global supply chains in recent years, and in recent months we have seen drought in the Panama Canal, conflict in the Middle East and terrorism in Red Sea and Persian Gulf chokepoints reduce throughput and create logistics backlogs. In response to and in anticipation of ongoing trade disruptions, firms are strategically retooling their supply chains from the “just in time” to the “just in case” model. This transition is still underway and has much further to go. Inventory-to-sales ratios remain below pre-Covid levels, especially among retailers as firms continue to contend with shortages and supply chain issues.

Figure 3: Inventory-to-sales ratios

Supply chain resiliency measures support logistics demand in other ways as well:

- Re-shoring and near-shoring: Sourcing product from North America-based providers eliminates the risk of transoceanic shipping disruptions. Increased domestic production in turn increases logistics demand from U.S. manufacturers.

- Location redundancy: Firms can improve the resiliency of their supply chains by diversifying their logistics locations and redirecting goods in response to disruptions. More logistics locations equates to more demand for logistics space.

- Rise of new logistics hubs: E-commerce, supply chain retooling, and geopolitics have also combined to give rise to new logistics hubs such as Charleston and Savannah, which benefit from upgraded port facilities, proximity to fast-growing Sunbelt markets, the expansion of the Panama Canal and disruptions to West Coast ports (but also face abundant supply pipelines). Texas border cities like El Paso capitalize on increased near-shoring and the USMCA trade agreement (which replaced NAFTA). South-Central Pennsylvania offers proximity to Mid-Atlantic population centers and a growing local manufacturing base. Very tight and expensive market conditions in Los Angeles/Inland Empire and the Bay Area have given rise to alternate locations in Reno, Stockton, Las Vegas, and Phoenix. Florida’s rapid population growth and connections to Latin America have elevated Jacksonville, Orlando, Tampa, and Miami as important logistics locations.

E-commerce is still driving logistics demand

The e-commerce penetration ratio of U.S. retail sales lags that of other countries, notably advanced Asian economies such as South Korea and emerging Asian economies such as China (Figure 4). Although the rate of e-commerce sales growth is slowing, our view is that U.S. consumers will continue to catch up in their online shopping habits to their counterparts in Asia and developed Europe.

Figure 4: E-commerce penetration, selected countries

Recent trends support America’s ongoing post-Covid adoption of e-commerce: online sales during “CyberWeek” (the five days after Thanksgiving) in 2023 rose 7.8% year-over-year (Y-o-Y). For Cyber Monday (November 27, 2023) alone, online sales were $12.4 billion, up 9.6% Y-o-Y. Traditional retailers increasingly drive online sales growth, with online sales accounting for 19% of Target’s total sales, 14% of Walmart’s total sales and 33% of Macy’s/Bloomingdale’s total sales (Figure 5). Reverse logistics—where 3PL firms handle product returns, which are estimated at $173 billion for the 2023 holiday season—also supports the need for more logistics space.

Figure 5: 2022 online sales as % of total, select retailers

With Euromonitor forecasting that the U.S. e-commerce penetration rate may top 30% before the end of the current decade (and still lag countries like Korea and China on this indicator), we expect e-commerce businesses, the online sales channels of regular retailers and the 3PL firms which support them to continue being a major source of logistics space demand for years to come.

Construction starts have plummeted

Soaring interest rates and tight credit conditions have curtailed logistics construction. Logistics starts have fallen dramatically from 180 million sf in Q3 2022 to 42 million sf of new starts in Q4 2023, which was the lowest in a decade (Figure 6), matching construction activity in the immediate aftermath of the GFC. Under construction logistics space has also decreased from record levels, leading to an expected period of relative undersupply after the current slate of projects delivers in 2024. High-quality new logistics product delivering in 2025 and 2026 will likely face limited competition.

Figure 6: Construction starts and supply underway (sf millions)

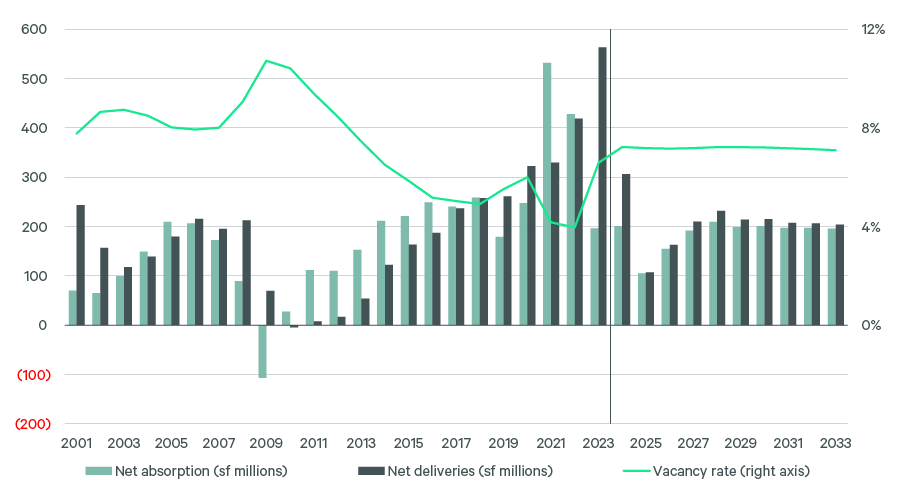

Structural factors are also limiting new logistics construction, notably the rise of NIMBYism and zoning challenges, higher land and construction costs and fewer available lots. CBRE Investment Management’s forecast expects logistics construction of around 200 million sf per year, consistent with the 2014-2019 period and well below the 560 million sf delivered in 2023. The reduced supply of logistics space and our outlook for economic growth, combined, result in our Q4 2023 forecast of stable vacancies at just above 7% nationally as shown in Figure 7.

Figure 7: U.S. logistics supply, demand, and vacancy forecast (sf millions)

Legacy logistics space is increasingly obsolete

Technological innovations that have boosted demand for modern logistics space have also hastened the obsolescence of older legacy logistics facilities. As shown in Figure 8, all older vintages of logistics properties lost occupancy in 2023 as demand flowed to the newest properties.

Figure 8: Annual net absorption, by vintage (sf millions)

Upgrading legacy logistics facilities presents challenges that often render such projects economically non-viable. Replacing floors requires emptying the facility and usually removing the existing floor since concrete does not adhere to concrete. However, adding floor strength often reduces the clear height to a non-standard measurement, potentially impacting the occupier’s racking system. Increasing the roof load presents similar challenges and often requires tearing off the existing roof. Because of these costs and challenges, since 1999, more than 400 million sf of legacy logistics space has been demolished to make way for other uses.

Fundamentals support above-trend income growth

Asking rent growth slowed in 2023 after rising by more than 20% in 2021 and 2022. Altogether, asking rents are up 55% from 2019, easily the strongest four-year period of growth on record. CBRE Investment Management’s latest forecast, driven by quantitative models that account for vacancy levels and trends, predicts rent growth averaging 3.5%-4.5% for the modern logistics sector, which ranks as the strongest rent growth forecast across the 13 sectors we track in the U.S. (Figure 9).

Figure 9: Market rent growth by sector, % annual average for 2024-2028

These figures relate to asking rents unless indicated differently:

* M-Rev PAF change per Green Street Advisors.

** Average daily room rate (“ADR”)

*** NCC denotes Neighborhood and Community Centers.

For illustrative purposes only. Based on CBRE Investment Management's subjective views and subject to change. There can be no assurance any targets or business initiatives will occur as expected. Forecasts are inherently uncertain and subject to change.

Other factors support ongoing strong income growth for logistics investments. CBRE reports that leases signed in Q3 2023 feature lease escalations averaging 3.6% per year. Owners can reasonably expect to double or even triple rents as pre-Covid leases mature and space is re-leased at much higher rent levels.

Cap rates are peaking

Transaction cap rates for logistics assets are up approximately 200 basis points from the record lows in 2022 because of the Fed’s rapid rate hikes and higher 10-year Treasury yields (Figure 10). With inflation moderating, the Fed has signaled—and markets are predicting—rate cuts this year. The 10-Year Treasury yield has retreated, and the surge in REIT pricing indicates a shift in investor sentiment.

Figure 10: U.S. logistics cap rates and forecast

We believe the higher cap rates offer a compelling value proposition. Lower interest rates and a return of liquidity should lead to cap rate compression over the next five years. Importantly, we believe cap rate trends for modern and legacy logistics product will diverge in the years ahead as occupiers increasingly require facilities which can accommodate the latest efficiencies and sustainability technologies. We believe the cheaper pricing combined with still-strong long-term fundamentals make 2024 a compelling vintage year.

Modern logistics forecast to deliver best total return

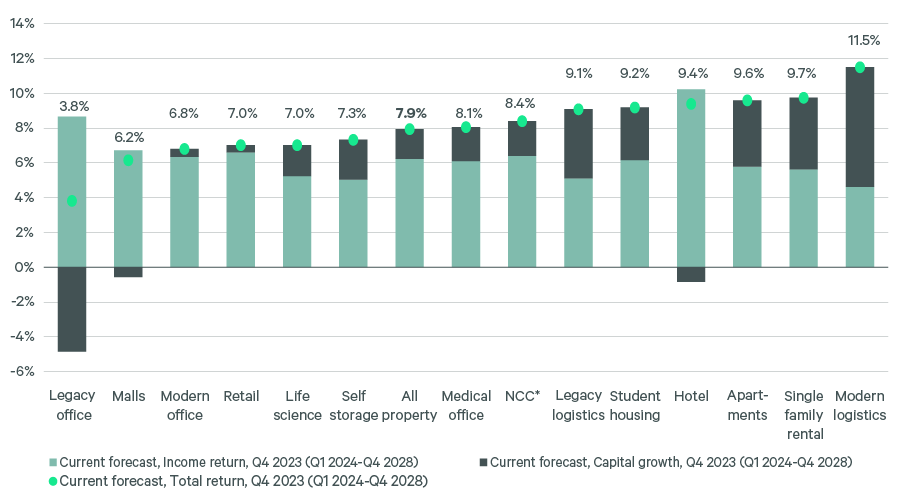

On a go-forward basis from January 2024, modern logistics is in the top position in our five-year core, unlevered total return forecast. As with all property types, the rising interest rate environment of 2022 and 2023 brought down returns in 2023. However, logistics outperformed other sectors on a relative basis given the still-strong income potential of the logistics sector and the amount of capital seeking to increase exposure to the sector. The 11.5% per annum (p.a.) total return forecast for modern logistics in the coming five-year period and the 9.1% for legacy logistics (see Figure 11) reflect significant embedded rent uplift as well as ongoing above-trend rent growth and, for modern logistics, cap rate compression.

Figure 11: Total return and return attribution by sector, average annual return for 2024-2028

Conclusion

We believe the structural factors that drove the extraordinary performance of logistics during the pandemic remain broadly in effect. E-commerce adoption continues to grow as consumption outpaces other parts of the economy and more traditional retailers expand their online operations. Disruptions to trade necessitate safety stocks, greater redundancy in logistics locations and near- and re-shoring of production. Migration patterns have boosted demand in secondary logistics locations. Each of these drivers support structurally higher logistics demand going forward.

Demand will increasingly favor modern logistics facilities that can accommodate increasingly sophisticated operations that rely on AI, robotic automation, electric vehicles and other technologies. Dependence on these technologies will hasten the obsolescence of most legacy logistics space, with the primary exception of increasingly rare well-located infill locations in major markets.

Near-term risks to the logistics sector may include short-term oversupply of space, rising vacancy rates and stalled rent growth. Construction starts have plummeted, presaging a period of relative undersupply in 2025 and 2026. As the current supply wave recedes, we expect vacancies to stabilize at levels supportive of above-trend rent growth. Moreover, embedded rent growth and 3%+ rent escalations will drive significant NOI upside as well.

Cap rates above 5% offer a compelling—but likely fleeting—entry point to the sector. The moderation in interest rates and recovery in REIT prices suggest that logistics values are nearing a cyclical low. CBRE Investment Management’s outlook predicts 2024 vintage modern logistics investments will top all sectors, realizing total gross unlevered returns of 11.5% per year, driven by strong income growth and cap rate compression. Legacy logistics total returns, supported by significant rent upside, are forecast at 9.1%.