Investment Perspectives

Positioning Ahead of a New Cycle in Listed Real Assets

By: Jon Treitel, CFA, Senior Director, Portfolio Strategist

July 16, 2024 4 Minute Read Time

Listed real assets markets offer investors an opportunity to capitalize on dislocated market pricing with secured access to next-generation assets. Several macro trends are coalescing to create an opportunity for investors to gain attractive entries at discounts to private market values. These secular growth trends increasingly require both real estate and infrastructure solutions at a scale optimally sourced in listed markets.

The coming monetary policy shift

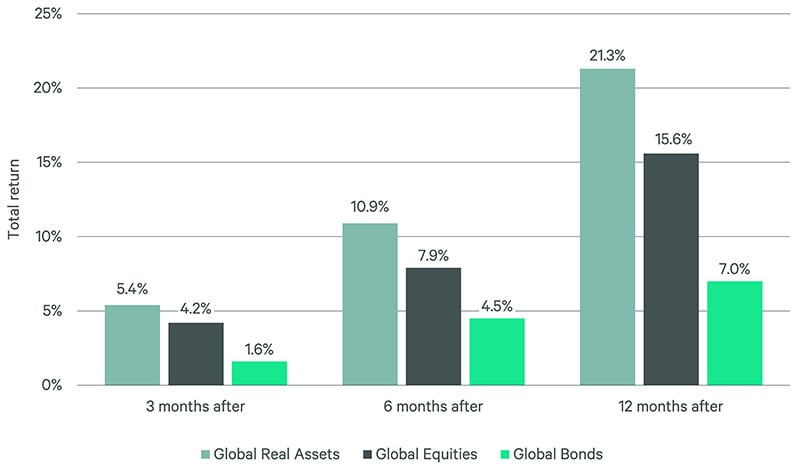

Over the course of the last global central bank hiking cycle, listed real assets exhibited a high correlation to bonds, a significant deviation from their long-term trend. In 2022 and the first three quarters of 2023, listed real assets suffered nearly two-years of negative returns, underperforming private real assets, broad equities, and, in our view, overshooting to the downside. We believe the end of the hiking cycle can provide a further catalyst for listed real assets to outperform. Recent trends support this thesis. In late 2023, after the Fed signaled its hiking cycle had peaked, listed real assets strategies significantly outperformed private markets for the final quarter and, as a result, the calendar year. For investors that believe this historical trend will repeat when the Fed begins easing monetary policy, it creates a window of opportunity to strategically position in listed real assets for what we believe will be an extended upcycle of outperformance.

Following the end of the Fed tightening cycle, listed real assets historically outperformed broad equities and bonds

Listed real assets after Fed pauses

We believe now is the time to invest in listed real assets. Listed real assets present both discounted valuations and accelerating growth opportunities. Successful navigation of the opportunities in listed real estate and infrastructure requires the reach of a global investment platform, cross asset class expertise, and a deep understanding of listed market exposure to capitalize on both secular long-term trends as well as short-term pricing dislocations.

In this article, we outline some high-conviction investment ideas that are driving positioning in our listed real assets strategies.

Powering generative AI

Surging interest in Generative AI (Gen AI) is reshaping our interaction with technology and the growth profile of real assets. Large-scale listed infrastructure and real estate are essential to meet the escalating demands of Gen AI—particularly in supporting the growth of data centers and their ever-increasing clean energy needs for power and cooling. An embryonic secular growth story blurs the boundaries of traditional real estate and infrastructure.

Data centers are facing capacity constraints and increased power and cooling requirements, which, in turn, are boosting pricing power and profitability for those listed companies managing those assets. Similarly, the power consumption in data centers is rising dramatically—estimated at 20-100 times more than traditional uses—which places unprecedented demand on utility providers. Major U.S. utilities have more than doubled their expected power demand five-year growth forecasts due to AI. Increased investment is required to meet escalating demands and enhance long-term earnings growth potential. As a cascading impact, renewable energy developers are experiencing surging demand for sustainable energy for existing data centers and meeting the needs of data center developers aiming to reduce carbon footprints.

For investors seeking exposure to these themes, listed infrastructure has been overlooked and undervalued. Through investing in companies with contracted and regulated return structures that are less susceptible to market volatility, listed infrastructure offers the potential for stable returns. As the global economy continues to integrate AI technologies, physical infrastructure—like data centers, renewable/low carbon power generation and transmission assets—becomes more critical. In the intersection of old economy assets with new technological demands, a unique investment opportunity has emerged combining stable returns while meeting innovation. Investors can capitalize on this thematic in listed markets with a distinct advantage, providing entries at a discount to private market values with scale.

Positioning for value and growth

Investors allocate to listed real assets to access quality assets and the potential for strong total returns girded by growing income and compelling sector exposures. Listed real assets managers can optimize portfolios with an eye toward both secular growth and current valuation opportunities, while dynamically managing markets to outperform passive options.

Our investment approach considers specific themes that are expected to endure over extended time periods and proactively responds to opportunities. For example, in listed infrastructure, we saw an opportunity to sizably increase holdings to utilities at the end of 2023, following their worst relative performance to the broad market in several decades, a discounted valuation set-up, and the emerging need for increased power and the likelihood of increased capital investment. For our listed real estate strategies, in the summer of 2023, we saw an opportunity to modestly re-invest holdings in office, after companies were trading at sizable double-digit discounts to our assessment of private market values. This short-term allocation allowed us to shore up an underweight allocation at extremely discounted pricing.

Investing where the trends converge: Views across real estate and infrastructure

Notable sector dynamics in real assets include:

- Renewable energy developers: The focus on clean energy and sustainability presents a long-term tailwind for this sector. However, valuations for renewable energy developers have been compressed in recent years relative to public markets. We believe this presents an attractive entry point for investors seeking exposure to this high-growth thematic. In the first quarter of 2024, private market participants validated this view with sizable purchases of listed renewable assets.

- Cell towers and communications assets: High interest rates have significantly compressed valuations and created a buying opportunity in this sector. Large U.S. cell tower assets have privatized at double-digit premiums to their listed market valuations, highlighting the potential disconnect.

- Single-Family Residential: Our strategies have been overweight single-family for rent, a sector which has recently benefited from take-private activity. In January, Blackstone privatized a large single-family for rent portfolio at a significant premium. The take-private activity illustrates that assets are undervalued in the listed market, which private capital is motivated to acquire at premium valuations.

- Storage Sector: The storage sector benefits from a host of forces, including demographics, and has proven to be resilient during economic uncertainty. Storage assets offer attractive discounted valuations relative to the normalizing growth that these operating businesses have the potential to generate over time.

Conclusion

The aftermath of this historic central bank hiking cycle has set the stage for a potential new return regime for listed real assets driven by discounted valuations and accelerating growth. Our active strategies seek to outperform through an awareness of both long-term growth potential present-day and valuation. As we look ahead, we see an opportunity for investors to position for a new upcycle in listed real assets.