Market Research

Optimizing U.K. Housing Strategies to Balance Impact, Risk and Return

By Alex Lund, CFA

February 26, 2024 10 Minute Read Time

“The U.K. housing crisis” is a phrase now synonymous with the 2020s. Decades of underbuilding and insufficient funding have led to a housing problem which often feels insurmountable. There is now a structural imbalance between housing supply versus need. Affordability pressures have become nationwide, rather than purely an urban concern. Added to this, in our view, new supply is frequently not being delivered where it’s needed most, both in terms of location and target demographic.

We believe more private sector capital is required to help plug the supply gap, but for new investors entering the sector, the landscape can look complex. While it’s tempting to take a relatively broad view of U.K. investment opportunities, by drilling deeper into the residential universe, it becomes clear that there is no one-size-fits-all housing solution. Instead, there exists, in our opinion, a multitude of specialist tenures, each with varied scale and impact potential and each with different risk and return profiles.

There is no denying that almost every part of the U.K. housing market is undersupplied, but investors approaching the sector need to carefully consider how they balance their risk and return expectations, while maximizing the potential impact of their capital. This paper aims to explore and help better define the U.K.’s residential universe, and offer guidance around how to shape an optimal investment strategy.1

The affordability crisis is now nationwide

The last three years have been one of seismic change for the housing market. A once in a generation cost of living shock has collided with a once in a decade shift in monetary policy. Working populations have physically shifted, spreading out from larger urban metropolitan areas to trade in proximity to work for more abundant space. At the same time, fewer tax incentives and evolving energy requirements make owning and renting residential property more challenging for the traditional buy-to-let landlord. The result is that private market rental growth is now trending at a level three times above its long-term average, well beyond any previous record.

Figure 1: Rent to income ratio

Rising affordability pressures are not new. Perhaps most surprising though is just how widespread these pressures have become. Of the nearly 400 local authorities in the U.K., 44% have a median rent to net income ratio above 35%, the typical threshold at which rents start to become unaffordable.

For renters, balancing these cost pressures has become increasingly untenable. For investors entering the sector, the implication is two-fold. Firstly, in our view, the emphasis should be on building scale in more affordable residential tenures. Investment strategies need to be nationwide, but with a local focus, while ensuring new housing works best for each local demographic and target market. Secondly, investors must balance housing need with their responsibility to deliver long-term inflation-protected income and minimize risk throughout market cycles.

Building scale on a ‘needs’ basis

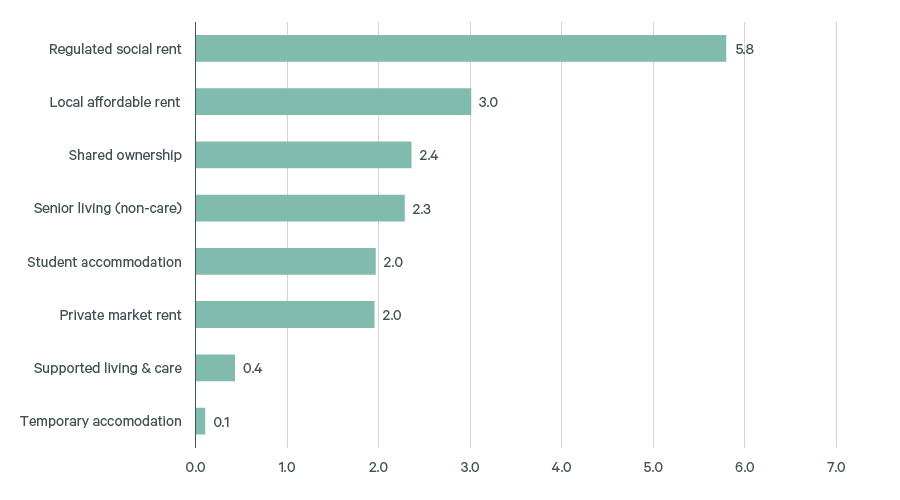

The scale of the investment opportunity within each housing tenure is a function of the underlying demand pool. A larger tenant or owner pool not only indicates greater occupier demand from a financial perspective, but also greater potential impact from a social perspective. Mapping the U.K. residential universe can illustrate how an investor approaching the sector can begin to think about portfolio positioning.

Figure 2: U.K. renter demand potential (million households)

Local affordable rent is a proprietary term defined by CBRE Investment Management reflecting rent affordability to local median incomes.

To quantify the demand and impact potential, we’ve broken out rental households into eight tenures across the residential spectrum. Multi-family and single-family then form the products with which these tenures can be delivered, with multiple segments often mixed together in one scheme to create a more diversified income stream.

Our analysis shows that the bulk of tenant demand sits in the regulated social and affordable rent segments. These two segments combined comprise half of the total rental pool across the U.K. For regulated social rent, this recognizes the 4.6 million households already in social housing, with a further 1.2 million households on waiting lists. By comparison, with the average market rent in the private rented sector (PRS) now close to £1,250 per month, we estimate that 61% of private renters are unable to afford this.2 In fact, a household would need to earn over £49,000 gross income a year for this to be affordable. Of the 39% of households who could afford this rent, categorized as ‘private market rent’ above, they formed only the sixth largest demand pool.

Inevitably, this pool of private renters shrinks further when factoring in higher rented, highly amenitized build-to-rent (BTR) schemes aimed at a more affluent demographic. In our view, the demand pool for regulated social and affordable rented properties, however, is only likely to grow larger as incomes fail to keep up with rental growth in the PRS. This should make scaling the investment potential here significantly easier, with affordable housing tenures expected to form an increasingly core component of residential portfolios as the market evolves and matures.

Factoring in impact potential versus risk and return

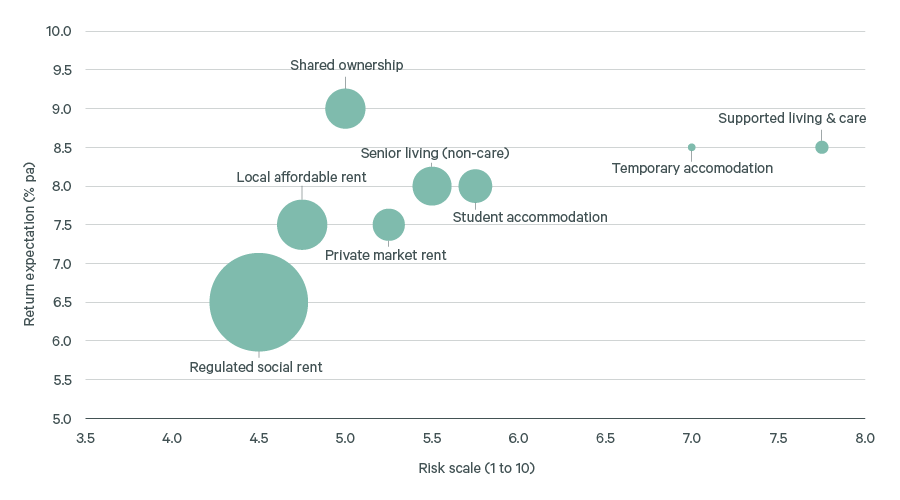

Overlaying the impact potential with our own estimates of risk and return expectations adds another layer to the allocation framework.

Figure 3: U.K. residential universe: risk, return expectation, and potential demand pool

Local affordable rent is a proprietary term defined by CBRE Investment Management reflecting rent affordability to local median incomes.

We’ve assessed risk based on seven key factors.3 On this spectrum, regulated social rent sits at the bottom end for risk, with supported living & care at the top. The lower risk exposure for regulated social rent is largely driven by the depth of the underlying occupier base, extremely low vacancies and its long-lease inflation-linked rental growth. As we move up the risk curve, leases tend to get shorter, turnover is often higher, leading to higher rental volatility. Operational intensity also increases, particularly for serviced-driven tenures such as student housing, supported living and high-end private market rent. Our performance expectations are then closely tied to these risk elements, factoring in market pricing and growth potential to build a forward-looking estimate.

Combining these three factors together—risk, return, and impact—we can begin to shape a portfolio that both meets an investor’s performance requirements and maximizes the positive impact of their capital. While maximum scale and social impact can be achieved by targeting the regulated rent sector, there is a clear opportunity to diversify across the investment universe, targeting complementary tenures with accretive risk-adjusted returns. Allocating across this spectrum should ultimately drive a more wholistic approach to a housing investment strategy.

Optimizing allocations to reflect local market need

The analysis above identifies nationwide needs, however, implementing a local place-based strategy requires analysis that goes deeper into the specific needs of a defined local area. In our view, a simple copy and paste of a nationwide top-down strategy is unlikely to provide the optimal balance between financial return and impact at the local market level.

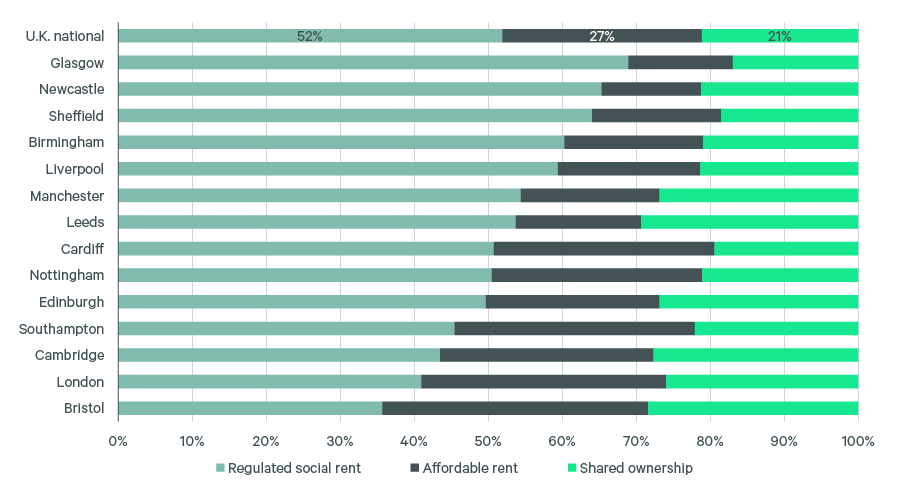

Figure 4: Allocating on a local ‘needs’ basis

Drilling into the three largest demand pools, we can begin to adjust our target allocations to better meet this need. At the broader city level, there is an obvious difference in housing demand between markets, like Glasgow and Bristol for example. Glasgow has one of the highest numbers of social housing tenants outside of London, nearly double that of Edinburgh. With comparatively cheaper market rents, however, the city requires fewer discounted affordable units. Bristol by comparison, has some of the highest market rents regionally, at close to £1,500 per month on average. While there is still a need to add to and improve the regulated social housing stock in Bristol, increasing affordability pressures in the private market underpin a larger demand pool in the city for discounted affordable housing.

Breaking this down to the postcode level can further identify how these factors vary by submarket and where the need for affordable housing is greatest. Analysis of Southampton shows two submarkets (SO19 and SO16) dominate in terms of potential demand for regulated social rent. The next largest postcode (SO15), however, shows a higher need for discounted affordable apartments, with rents there a third higher than the Southampton average. We see a strong correlation between demand for all types of affordable housing versus levels of deprivation, income inequality and limited access to local services.

Figure 5: Southampton postcodes—demand potential by households & deprivation index

Overlaying this data with local housing waiting lists, affordability metrics, and the quality of existing housing stock can build a much clearer picture of the market. While top-down data can never substitute the need for ground up expertise, collectively this framework can help optimize a local impact strategy. Understanding the occupier base in this way should equally lead to improved financial performance, while minimizing specific risk at the asset level.

Conclusion

The investment opportunity across residential now forms, in our view, a significant and growing part of the U.K.’s investible universe. But building an optimal residential portfolio needs to be consumer-led. Going back to basics and focusing on the underlying occupier need shows the importance of balancing impact potential with an investor’s risk and return requirement. The three factors of risk, return and impact are inextricable linked in driving long-term sustainable returns. Delivering new affordable housing which caters to each submarket and target demographic, not only maximizes the social benefit of invested capital, but means investors are rewarded with a more resilient and growth-oriented occupier base. Getting this balancing act right, in our view, is the first step in optimizing an investor’s risk-adjusted performance.

1 This does not constitute investment advice and you should consult with your financial adviser for any advice in relation to such.

2 Based on 40% of household disposable income

3 Occupancy, lease length, rent volatility, operational intensity, regulation, reputation, and liquidity.