Market Research

Navigating Distress and Opportunities in Germany

By: Sehr Nawaz, Insights and Intelligence

June 19, 2024 5 Minute Read Time

Introduction

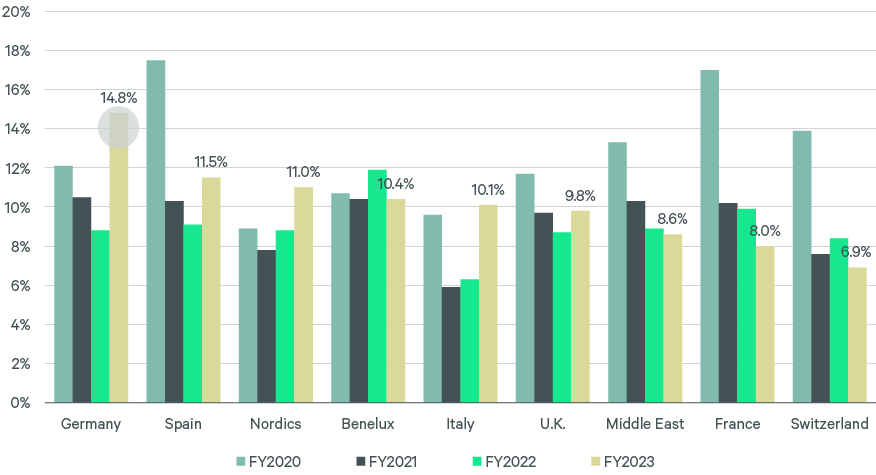

Looking back at 2023, it would be difficult to discuss Europe’s economic fate without referencing Germany in some respect. Germany emerged as the most distressed market in Europe, influenced by rising interest rates, deterioration of the investment market, liquidity pressures and stagnant profitability, which has persisted since the start of 2023.1

Macro headwinds include weaker global trade which continues to hurt German exports along with high energy prices impacting energy-intensive production. Debilitated trade is exacerbated by increased competition from China, particularly in the automotive industry.

Figure 1: Distress levels (as a % of companies)

We believe these macro challenges are more cyclical than structural and sit alongside heightened geo- and domestic political tensions, including the rise of the far-right Alternative for Germany (AfD) party. Economic activity dragged as a result, with GDP falling 0.3% in 2023. Inflows into Germany open-ended property fund turned negative in 2023 with many funds becoming net sellers, revealing liquidity challenges and signs of distress. These challenges are especially visible when looking at debt markets. With approximately one third of commercial real estate loans in Germany facing higher borrowing costs over the next three years, the risk of credit defaults has risen.2

Despite this apparently bleak picture, we believe there is also considerable opportunity. As many investors struggle to refinance their debt and look to raise cash, we expect an increased level of assets will be sold on the market creating opportunities for investors to take advantage of attractive pricing. The market has experienced persistently strong rent growth and clear signs of an economic recovery as inflation falls and GDP growth looks to stabilize in the near term. This paper will explore these themes with a focus on the residential sector.

Liquidity

Threats

German open-ended mutual property funds saw five consecutive months of net outflows at the end of 2023, as investors withdrew a total of €1.1 billion over this period.3

This contributed to a broader slowdown in German investment volumes in 2023, totaling €31.7 billion, 52% down year-over-year (Y-o-Y) and almost 60% down from the ten-year average.4 The most impacted sector was offices, totaling just under 17% of total transactions at the end of 2023, compared to an average of 38% over the last ten years.

Figure 2: German open-ended monthly net flows, € billions

Opportunities

Many market participants expect central banks to start easing this year as seen by The European Central Bank’s recent accouncement of a 25-basis points (bps) reduction in the bank’s key rate, which would improve the uncertain investor sentiment that has plagued the German market in 2023.

Interest rates, however, are expected to stay high relative to the post-GFC period. With many investors needing to repay or refinance debt before approaching deadlines, some will seek to sell assets. This should create opportunities for active investors to acquire assets at attractive pricing.5 This said, Germany is not experiencing full distress; investors, therefore, will need to be both more selective and more realistic in their valuations to take advantage of the current situation. With 10-year government bond yields expected to move inwards and stabilize around 2.3% in Germany, we believe that the coming quarters will provide an attractive window to deploy capital into a very core market like Germany at unusually elevated yields.

Energy

Threats

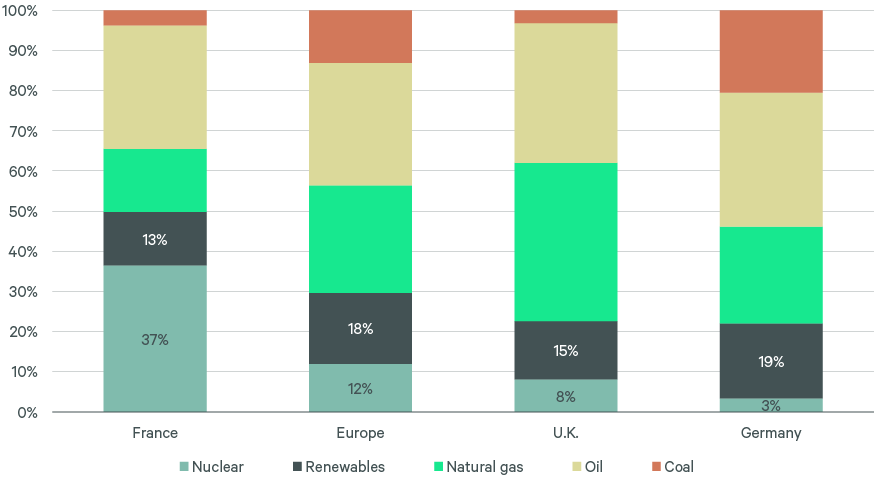

Russia’s invasion of Ukraine led to heightened energy costs in Germany due to its significant dependance on fossil fuels from Russia. Germany has replaced fossil fuels from Russia by other sources over the recent years, such as by liquid natural gas which is delivered by container ships via the Baltic Sea at a higher cost, in turn restricting industrial activity. The chart below shows German dependence on coal to be higher than the European average and fossil fuel sources dominating Germany’s energy supply mix.

Figure 3: Total energy supply mix (%)

Despite the government’s attempt to contain rising energy costs with gas and electricity price caps, the number of households living in energy poverty—spending more than 10% of income on energy—has risen steeply since the onset of the energy crisis in Europe in 2022.6 The knock-on effects have led to a squeeze on household disposable income and weaker consumer spending, with particular pressure on residential tenants. This is further exacerbated by continued rental growth across the major German residential markets, ranging from 4% to 8% Y-o-Y in 2023.

Opportunities

Despite falling capital values in the residential sector across major German cities ranging between 15%-25% over the same period,7 recovery is underway with signs of stabilization on the horizon. Looking at the historical context, energy costs have fallen 30% in Germany since the peak of the crisis 12 months ago where we saw rapidly increasing costs for heating, electricity and transport fuels.8

The transition process to meet climate goals means that over 60% of existing housing stock needs to be renovated in the next decade to meet EU targets, creating opportunities for investors to acquire older stock at discounts and lead the renovation process. This is reinforced by the fact that many buildings in Germany have been constructed before the 2000s and are potentially vulnerable to becoming obsolete. Improvements in sustainability performance should also help to unlock rent revisions in older stock. Timing is key, with the more attractive discounts available to investors in the short term, before markets start to recover and values begin to rise.

Figure 4: Risk of becoming obsolete assets by 2033

Construction

Threats

Higher energy prices, along with increased financing costs and deteriorating development economics, have impacted construction activity, leading to severe delays on many development projects or even complete halts. Some developers have been pushed into insolvency as bank financing dried up and their financial woes grew. German research house, DIW Berlin, forecasts construction spending to shrink by 3.5% in 2024 to €546 billion,10 which would be the first decline since the 2008 financial crisis. The residential sector is impacted by this the most. With building permits falling by almost 27% in 2023 and vacancy already sub 1% in major cities, real issues of longer-term affordability are growing.

Figure 5: German Construction spending in € billions

Opportunities

Despite a troubling year for construction in Germany, with interest rates considered to have peaked , we believe construction costs should begin to fall as we enter the next cycle. That said, there remains a window of opportunity to target developers still facing distress in the short term—with many emerging from the challenges of last year.

Longer term, there are planned subsidies to build 100,000 social housing units and 60,000 new affordable homes to accommodate those in desperate need, as well as a relaxation of building standards to ease the costs of construction and overall process.11 This should provide greater opportunities for residential investors looking to access the German market.

Especially for German housing stock that was built before 1979 and in need of capex for renovation purposes, prices have fallen around 14% since the peak in 2022 compared to new buildings which saw less capital depreciation of around 5%.12 This creates opportunity to acquire and upgrade stock at lower prices without the need to commit to more intensive development.

Conclusion

2023 was undoubtedly a challenging and testing year for the German real estate market, but we believe that the market is now broadly bottoming out and that most of the downturn both in terms of pricing and transactions are behind us. The recovery is likely to be gradual in 2024 and it will not be until 2025 where we will begin to see more significant upside. As always, market timing is key with distress never present forever. It will be those investors who are ready and active in the market that are able to take advantage of the best discounted pricing seen in decades in what is Europe’s largest and most core market. It is for these reasons, and despite the negative perception of the economy, Germany screens attractively in our risk-adjusted return outlook and takes a clear overweight position in our latest European model portfolio.

2 Bloomberg, Rising Distress in Germany Signals a Lot More Struggles Ahead, Bloomberg.

3 REFIRE: German Real Estate Finance: German open-ended funds confront a tidal wave of withdrawals, REFIRE (refire-online.com).

4 JLL, Q4 2023 Investment Market Overview Q4 2023, JLL.

5 JLL Q4 2023, Investment Market Overview Q4 2023, JLL.

6 Clean Energy Wire: Energy costs for German households drop 30% since height of energy crisis – analysis | Clean Energy Wire

7 CBRE ERIX Data, Q1 2024

8 ECEEE: News (eceee.org)

9 ING, July 2023: The green transition takes hold of Germany’s property market | articles | ING Think

10 Reuters, April 2024: Outlook for German construction sector grim in 2024, researchers say, Reuters.

11 Reuters, April 2024: German builders demand billions in subsidies to stem housing crisis, Reuters.

12 ING, Germany’s housing slump finally looks to be ending | articles | ING Think