Future of Real Assets is Today

Many shall rise that have (relatively) fallen: The opportunity in listed real estate

December 15, 2025 8 Minute Read Time

Overview

Author

Senior Director, Portfolio Strategist

Author

Chief Investment Officer – Listed Real Estate

Prefer a PDF?

Over the last three years, global listed real estate has performed for investors with ~9% annualized returns.i However, its gains pale in comparison to broad equities, which delivered returns over 2.5x that level. Looking ahead, we see an opportunity for listed real estate to reaffirm its long-term track record of outperformance.ii We expect outperformance to private markets to continue, and for the asset class to deliver resilient, income-enabled returns. As we review the outlook for global real estate, we find:

- Listed real estate as a likely beneficiary of broadening market participation and the search for resilient income.

- A likely advantage for global exposures compared to U.S. real estate alone.

- Dynamism in REITs: portfolio optimization, privatization, and the potential for enhanced growth.

- An opportunity for active managers in improved asset class breadth and enhanced positioning.

A potential beneficiary of broadening market participation in REITs

While global real estate has returned ~10% in 2025, it still has lagged broad equities. We believe REITs can be a key beneficiary of broadening market participation. Valuations are compelling: as earnings have been resilient, the relative valuation gap between global real estate and broad equities stands at levels last seen in the aftermath of the GFC and the COVID-19 pandemic.

Relative valuation for listed real estate nearing historic levels

Relative 12-month forward P/E multiples (Global real estate vs. MSCI World)

Following similar periods, REITs have historically outperformed—though the COVID-19 recovery was shortened by historic central bank tightening that began in March 2022. On average, when listed real estate has traded at a one standard deviation discount, it has averaged ~27% returns on a forward one-year basis.iii

The period preceding the 2000-2007 bull cycle for REITs was the most similar historical period to the current environment. Like that period, we are in the midst of an extended period of listed real estate underperformance relative to technology stocks, while investor enthusiasm for more resilient, less growth-oriented, earnings has diminished. We further see the likelihood for accommodative or range-bound long-term government bond yields in the future. We believe this combination of factors—recent underperformance, disconnected valuations and a sanguine “do-no-harm” environment from risk free rates—can allow REITs to reassert their long-term performance advantage compared to broad equities.

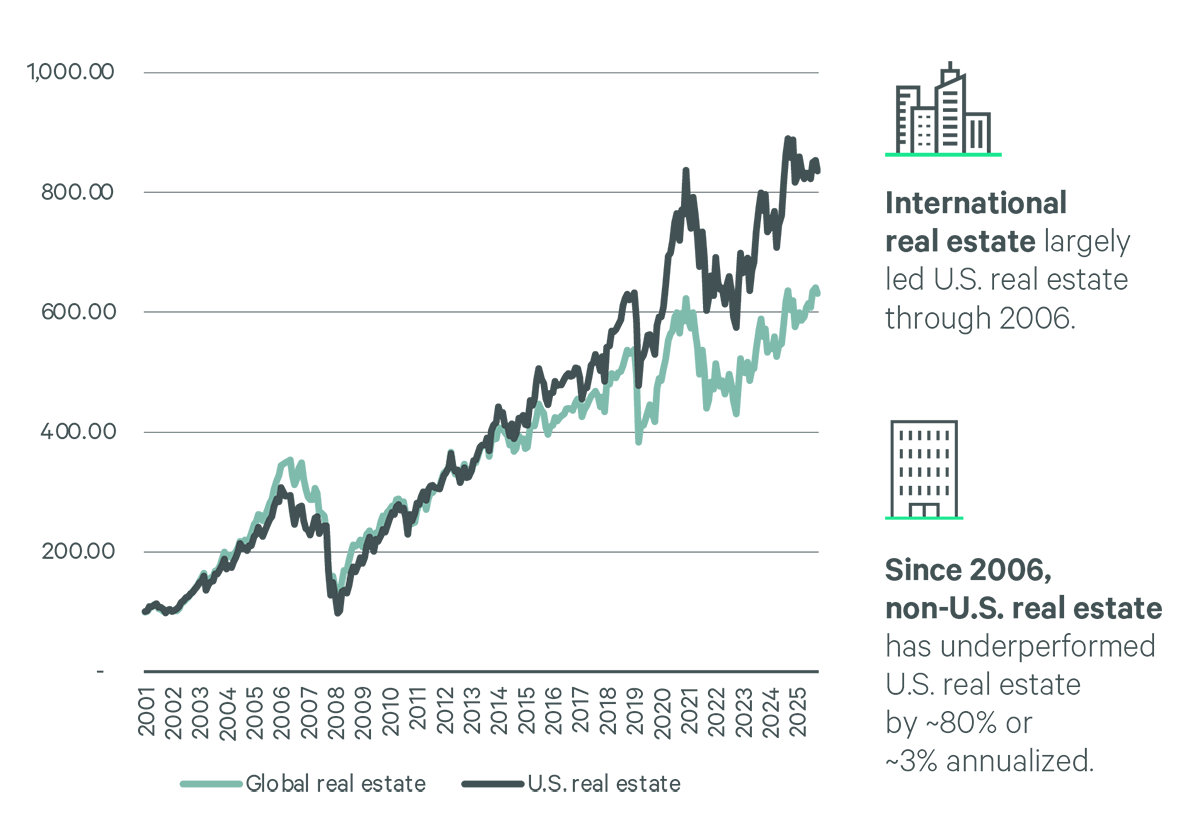

A continued advantage for global compared to U.S. real estate exposures

Global real estate has outperformed U.S. real estate thus far in 2025; we believe this trend will continue. Global growth is expected to moderately outperform the U.S. Global growth is being driven by the more recent eclipsing of higher borrowing rates, as well as the relatively earlier-growth stage of select “next generation” real estate companies at a global level. From the perspective of relative valuation, global real estate is trading at a greater relative price-to-net asset value (P/NAV) discount compared to its own history versus U.S. real estate.

We see the combination of relatively stronger growth trends and enhanced valuation as contributing to potential global outperformance. We believe global real estate can embark on an extended period of such performance— effectively reversing the trend seen since 2007.

Relative performance potential for global

Performance comparison

Dynamism in REITs: portfolio optimization, privatization, and the potential for enhanced earnings

Over the course of 2025, listed real estate companies have continued to optimize capital market activity to enhance their portfolios. On the acquisition front, high profile REITs in the private pay senior housing sector have announced over $25 billion in capital for accretive acquisitions, while listed companies with undervalued niche assets, such as marinas, have monetized their holdings at accretive levels to generate proceeds for deleveraging and special dividends. We see the potential for M&A activity and privatizations to rise. In the U.S. and Canada, select residential housing and diversified companies have embarked on strategic reviews, which have led to outperformance of those equities. In the U.K. and in Europe, live deal activity has trended above historical averages across the industrial, healthcare, residential and storage sectors. From a governance perspective, we also see enhancement in the quality of select global Japanese REITs, which have committed to revised compensation practices, share repurchase activity and enhanced transparency for investors.

When we review the asset class, we see multiple fundamental drivers supporting potential upside to our current growth expectations for REITs.

Sources of potential upside for listed real estate

Dynamism in management: Capitalizing on increasing breadth, dispersion and optimizing positioning

Coinciding with a concentration of market leadership in broad equities, we’ve also seen a concentration in market leadership for REITs. Below, we show the percentage of outperforming stocks in the FTSE NAREIT All Equity REIT Index. Recently, in mid-2025, this percentage bounced off historical trough levels.

Narrow leadership for broad markets has coincided with narrow leadership in REITs

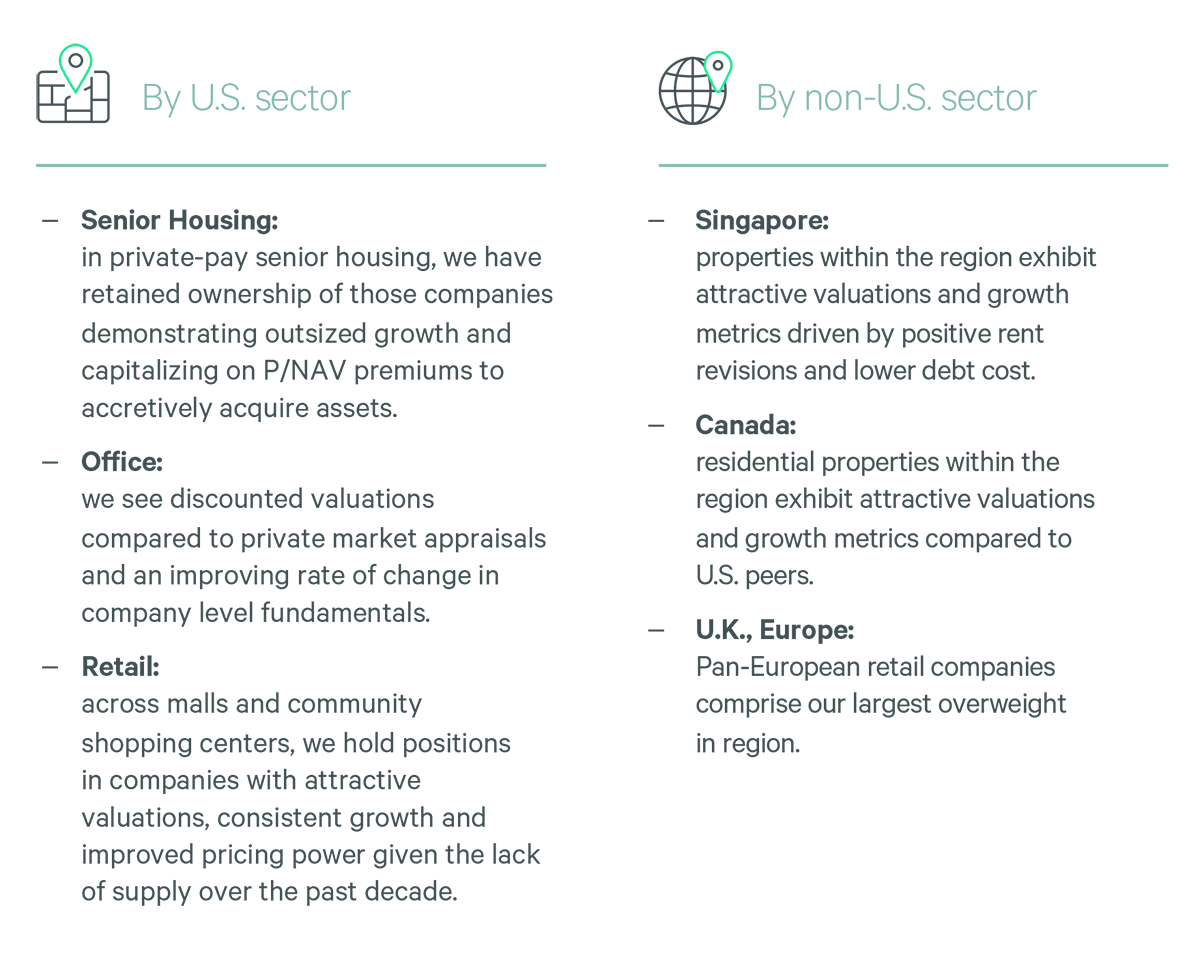

As listed real estate breadth improves, we believe that the opportunities for active management will be enhanced. We further believe that the fundamental metrics we value, and our approach to seeking positive exposures to growth, value, market and quality factors, will reassert its historical efficacy in driving performance. Our sector and security ranking is a dynamic process. Each week and month, we formally rank global real estate regions, sectors and securities on these metrics, and we develop optimized portfolios based on the inputs of our fundamental investment team. Our positioning reflects the views of our investment staff, which leverages the broader CBRE IM organization and our library of proprietary listed real estate metrics spanning back over four decades. As we consider the new year, notable positioning at the sector level includes a bias towards the following:

CBRE IM global listed real estate positioning (October 2025)

A restoration for listed real estate

As we look ahead to a new year, we believe listed real estate presents an opportunity for resilient income, compelling valuations, and total returns. An allocation to listed real estate can mitigate an investor’s risk from overexposure to relatively concentrated broad markets should the “rent come due” outside of real estate. We see further advantages for global real estate exposures and for active managers to enhance returns. As we look ahead, we are optimistic on the potential of the asset class and for our ability to enhance it.

ii Over the trailing 25 years ended October 31, 2025.

iii Represents periods between February 2005 and October 2025 where the FTSE EPRA NAREIT Developed Index traded at a one standard deviation discount to its historical average compared to the MSCI World Index. Source: CBRE Investment Management. Source: FTSE EPRA NAREIT Developed Index, MSCI World Index and FactSet as of September 30, 2025. Information is the opinion of CBRE Investment Management is subject to change and is not intended to be a forecast of future events, or a guarantee of future results, or investment advice. Forecasts and any factors discussed are not indicative of future investment performance.