Investment Perspectives

Four Opportunities in Modern Logistics

Investing in an Era of Unrelenting Disruption and Innovation

May 21, 2024 10 Minute Read Time

The logistics sector is in a transformative period driven by technological advancements, evolving consumer expectations, sustainability mandates and geopolitical complexities. These forces are redefining logistics real estate requirements and establishing new demands for occupiers in a rapidly evolving global commerce landscape. Operators are compelled to reassess strategies to remain competitive, efficient and profitable amid a tide of unrelenting disruption and innovation. Landlords and investors must equally adapt their investment strategies accordingly.

Investors seeking to achieve higher yielding development returns must deliver buildings that provide enhanced structural components to support robotics, material handling systems and solar arrays which amplify efficiency and generate ancillary power. Occupiers must navigate geopolitical complexities and manage intricate supply chains to meet the demand for ever-faster deliveries. Shareholders and lenders are increasingly focused on achieving net zero goals. The need for specialized logistics facilities to manage concurrent priorities is intensifying, which is blurring the lines between traditional real estate and infrastructure.

In this article, we will explore four opportunities that capture the growth potential and evolving needs of modern logistics.

1. Modernity versus legacy

Modern logistics facilities are purpose-built to meet the demanding requirements of today’s e-commerce giants, third-party logistics providers, global retailers and advanced manufacturers. The explosive growth of U.S. e-commerce—expected to account for 34.9% of total retail sales by Q4 2034—is a major driver for modern logistics facilities (Source: CBRE Research).

The rise in online sales has led to a greater proportionate share of annual costs being dedicated to maintaining omnichannel platforms, driving the need to reduce costs per item in warehouses. E-commerce fulfillment requires faster order processing and quicker delivery times. Modern facilities, with their advanced design specifications, are better equipped to integrate automation and robotics, resulting in significant cost reductions per item shipped. Evolving customer expectations and environmental regulations necessitate electrifying delivery fleets, requiring on-site electric vehicle (EV) charging stations which also pairs with material power requirements to run automated systems.

Key technical building specifications for modern logistics facilities include:

- Elevated clear heights: to maximize storage cubic versus linear capacity

- Enhanced concrete slabs: thicker slabs designed with increased structural steel to support heavy material handling equipment, robotics and automation systems, automation equipment and solar-paneled roofs

- Efficient column spacing: to facilitate automated product movement through warehouses

- Advanced infrastructure: such as sprinkler systems, on-site battery storage, additional conduit, upsized utility lines and EV charging stations

The rapid pace of technological innovation highlights the limitations of legacy logistics facilities. More than 72% of logistics assets in the U.S. were built before 2000, with over a quarter being more than 50 years old. Only 15% of total U.S. logistics buildings have been constructed since 2010. The Class A segment of the U.S. logistics market has accounted for 50% of the total net absorption since 2018. Retrofitting older facilities to meet modern logistics demands is challenging—they often fall short of the needs of modern tenants. Despite high space demand over the past 12-24 months amid tight market conditions, these shortcomings are becoming more apparent. The acquiescence to less than ideal space is temporary and the long-term demand for more suitable facilities is increasing. This supply-demand mismatch has created a bottleneck, channeling occupier demand into a highly desirable modern segment, which represents around 10%-15% of existing U.S. stock, underscoring the scale of the imbalance. The imperative for efficiency amplifies the logistics supply-demand imbalance.

Figure 1. Share of U.S. existing logistics properties by year built

Note: Logistics property type includes properties over 50,000 SF and with subtypes: warehouse, truck terminal, distribution, manufacturing, cold storage and no secondary type.

For illustrative purposes only. Current market conditions differ from prior market conditions, including during prior periods of stress and dislocation. There can be no assurance any prior trends will continue.

Operational and systems upgrades increase productivity and efficiency, improving profit margins with fewer facilities. For instance, in late March, UPS announced a plan they are calling, “Network of The Future,” to invest $9 billion in warehouse network upgrades, installing autonomous guided vehicles, automated sorting systems, robotics, and systems that prioritize processing customer requirements without human intervention. These upgrades will expand handling capacity by 30% to 35% and enable the closure of around 200 facilities over a five-year period, resulting in $3 billion in savings by the end of 2028. This initiative is similar to FedEx’s recently announced network transition called “Network 2.0.”

E-commerce growth trends, coupled with the need for operational efficiency and sustainability, have created a binary demand profile in the already bifurcated logistics space. The scarcity of modern facilities, combined with the limitations of legacy stock, has solidified the “modernity versus legacy” concept as our highest-conviction investment thesis in logistics today. There is a significant demand for new modern logistics development. Investors should focus on identifying national-scale developers with substantial balance sheet capacity to execute large-scale joint ventures across multiple markets.

2. Maker’s markets

The U.S. advanced manufacturing landscape is experiencing a resurgence, driving significant real estate demand from intellectually sensitive and high-skilled industries producing high-value goods and jobs. The federal government is actively promoting reshoring initiatives in high-tech manufacturing sectors, such as clean energy, EVs, battery-related lithium refinement, semiconductor chip manufacturing, medical biotechnology and life sciences. Policy support such as the CHIPS and Science Act, with over $200 billion allocated, aim to boost domestic semiconductor chip production. Similarly, the Inflation Reduction Act incentivizes companies to use domestically manufactured materials to support a clean energy supply chain.

These policies are motivated by the need to reduce dependence on China and other international manufacturers of advanced semiconductor chips, viewed as a national security and economic risk. Additionally, there is a focus on enhancing supply chain resilience amid geopolitical conflicts and climate change, which can lead to inflationary pressures. The vulnerabilities in supply chains were highlighted during the pandemic and geopolitical conflicts like Houthi rebel attacks disrupting vital shipping routes in the Red Sea. In January, attacks on ships forced automakers Tesla and Volvo Car to temporarily suspend production in Europe due to a shortage of components. Rerouting is causing increased transport times and costs while creating supply chain gaps. This situation underscores the urgency of reshoring critical manufacturing capabilities.

The government-supported reshoring trend has accelerated the rise of "Maker's Markets"—geographic clusters optimizing shared knowledge and resources. These self-selecting clusters amplify innovation but rely on advanced infrastructure to reduce transportation costs and lead times, sustainable energy sources, skilled labor and vibrant ecosystems. The Biden administration's deals with Intel and Taiwan Semiconductor Manufacturing Co (TSMC) to fund semiconductor chip production and research in Austin, Texas, exemplify this trend. Intel secured $8.5 billion in direct funding and $11 billion in loans, while TSMC agreed to US$6.6 billion in direct funding and $5billion in loans, cementing Austin’s status as a world-leading semiconductor manufacturing hub that creates thousands of high-skilled jobs.

The emergence of Maker's Markets is generating a broader user base for “best-in-class” facilities, growing the market for the logistics sector as existing operators expand and new entrants emerge. The influx represents a long-term tailwind for the modern logistics demand profile and rental growth outlook, as operators increasingly require strategically located modern logistics facilities to handle the increased volume, speed and complexity of advanced manufacturing supply chains. State-of-the-art automation, sorting systems and efficient layouts will be essential to manage the movement of materials, equipment and finished chips within these dynamic Maker’s Markets.

3. West Coast port primacy

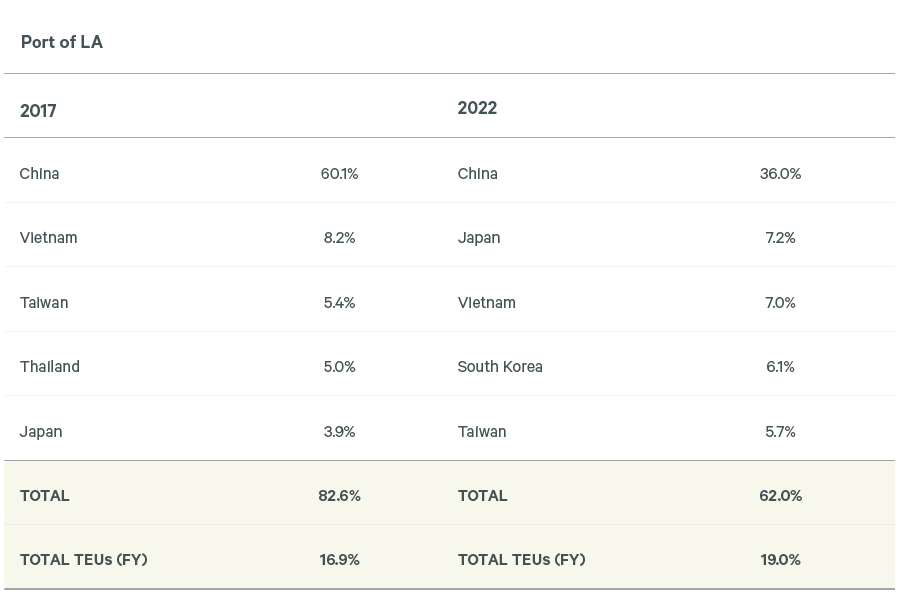

West Coast ports like Los Angeles and Long Beach (which combine as the San Pedro Bay Port Complex) are historically dominant for China-led Asian imports. These ports experienced a notable decline in cargo volumes post-2018. This weakness stemmed from various factors, including U.S.-China trade tensions with tariffs impacting the importing of Chinese goods, labor disputes causing port congestion, delays and stranded goods, alongside a strategic shift to reduce reliance on China leading to increased Southeast Asian imports, which caused cargo volumes to migrate to East Coast ports. U.S.-China trade tariffs during the Trump administration caused the proportion of China’s twenty-foot equivalent units of cargo volumes, known as TEUs, to drop from around 60% to 36% in the period between 2017 and 2022. Concurrently, as TEU volumes through the Port of Los Angeles from China dwindled, total volumes increased 12.4% to 19.0 million, creating a more resilient port supported by a more diversified pool of international trading nations. See table below.

However, recent trends suggest a resurgence in West Coast port activity. In February, L.A. imports surged by 64% year-over-year, with January imports reaching record highs. Similarly, neighboring Long Beach experienced a 24.1% year-over-year increase in container throughput and a 29.4% increase in imports during the same period. This renewed performance indicates that the post-2018 decline in West Coast port activity may be over. The return of West Coast port primacy reflects retailers and suppliers reworking distribution strategies to position goods closer to where consumers live, while capitalizing on advanced infrastructure and reliable trade partners. The normalization of West Coast imports at a higher level will support the occupier demand profile and rental outlook for the market’s logistics space. This bullish outlook hinges on significant supply chain infrastructure investments to enhance port competitiveness and sustainability, necessitating digitalization and decarbonization of the state freight sector.

In contrast, East Coast ports are facing more challenging outlooks. Climate change-induced droughts are impacting the Panama Canal, a critical artery for East Coast ports, affecting cargo movement between East Coast ports and international regions. Panama’s aging infrastructure is less predictable and is cost-prohibitive, tilting the balance in favor of West Coast ports. The impact of the Francis Scott Key Bridge collapse in Baltimore is still being assessed.

Logistics strategies are evolving alongside infrastructure needs. As operations become more sophisticated, the traditional boundaries between real estate and infrastructure are blurring. A useful analogy is a Russian nesting doll: the logistics company serves as the core, surrounded by selected technologies, buildings, location and ultimately, port infrastructure. Successful investment strategies integrate this interconnected landscape. For example, warehouses are evolving into mini infrastructure, requiring on-site power generation to meet rising energy demands for automation, robotics, artificial intelligence systems and electric truck fleets.

4. Air logistics markets

The air logistics market presents an often overlooked investment opportunity. Uncertainty plaguing global supply chains, stemming from geopolitical conflicts, trade tensions, climate change-related disruptions and aging infrastructure failures, is compelling operators to reassess their supply chain networks, prompting a surge in demand for air freight services.

Despite its higher cost compared to traditional ocean shipping, air freight’s unparalleled speed and reliability make it a valuable tool for managing variability in supply chains. According to data from Norway-based firm Xeneta, global air freight volumes have experienced double-digit growth for four consecutive months through March, particularly in trade lanes affected by the Red Sea crisis. In March, average shipping costs on key trade lanes rose significantly, with rates linking the Middle East and South Asia to Europe increasing by 46% compared to February. Although air freight is more costly than ocean freight, the speed of delivery is crucial for many companies, especially with ocean vessels now taking up to 10 additional days to circumnavigate the Cape of Good Hope in South Africa. Manufacturers are reportedly shifting high-priority goods from ocean to air “to meet production schedules and keep factories operational.” Beyond geopolitical concerns, demand is also driven by strong growth in Asian e-commerce companies that rely on aircraft to ship goods directly to consumers.

Taken together, we estimate that these factors could potentially double air freight usage from its current approximate 5% share of logistics solutions to 10%-15% over time. This trend underscores the need to focus on the wider supply chain and multiple channels by which goods are delivered between continents and inevitably to the end consumer.

Conclusion

The convergence of transformative forces is reshaping the logistics industry and the landscape for investment. The "modernity versus legacy" theme sits at the core of all the opportunities explored here. Each theme underscores the urgent need for cutting-edge logistics facilities tailored to the demands of e-commerce, automation and sustainability. A focus on efficiency necessitates not just new development, but a re-evaluation of existing assets.

Legacy facilities built prior to 2010 are simply not able to accommodate the demands of modern logistics users. The limitations in ceiling heights, column spacing and overall design specifications render them ill-suited for automation and technological integration. The rapid obsolescence of these facilities dramatically shrinks the total inventory of relevant assets for investors focused solely on traditional industrial real estate.

The evolving demand profile is blurring the lines between "industrial" and "logistics" product. Modern logistics facilities are miniature ecosystems, requiring on-site power generation, advanced infrastructure and even charging stations for electric vehicle fleets. These features fundamentally reshape the function of the building, pushing the definition beyond mere storage space.

The confluence of current factors creates a sense of urgency for investors whose thinking has shifted from asking, "Do I own industrial real estate?" to "Do I own logistics product that meets the demands of the modern supply chain?" Strategic alignment of logistics investments with these transformative forces positions investors to capitalize on the evolving demand trends for the years and decades to come. The future of logistics has arrived but many risk being left behind.