Portfolio Allocation

Europe’s Forgotten Middle: Where a Housing Crisis Meets an Investment Opportunity

June 3, 2024 7 Minute Read Time

This perspective is part of our Anchoring Your Portfolio with Real Assets series.

The problem of affordable housing for middle-income earners is a pressing issue often overlooked across Europe. The middle-income earner demographic forms the backbone of society—comprised of our nurses, teachers, police officers and firefighters—yet many are at risk of being priced out of the cities where they serve.

Affordability gap increasing

Throughout Europe’s housing markets, a persistent supply and demand imbalance has endured for decades. These dynamics have long-established a favorable risk-return investment thesis for the residential asset class. Over time, the diversification and lower-risk characteristics have improved as European residential markets have matured and become more liquid. In recent years, the residential investment thesis has broadened significantly beyond the traditional affordable housing focus to include the growing and larger housing shortage for the rising cohort of middle-income earners. The context of this market shift is understood, but the resulting opportunity is underappreciated.

Historically, housing development has struggled to keep pace with the rising demand spurred by population growth and urbanization. This decades-long demand surge has collided with financing constraints, escalating construction costs, disruptions in supply chains and tight labor markets. Together, these headwinds have blunted new housing development, at a time when demand continues to increase, supporting upward pressure on open market rents and exacerbating the affordability crisis among middle-income earners. At the same time, high interest rates have pushed homeownership increasingly out of reach for many, fueling a growing urgency for new affordable rental options for the squeezed middle. Two real-world consequences of these housing trends have emerged. First, the absence of housing options for middle income earners fosters a social divide within cities as the income gap widens. Second, cities function at a suboptimal level when key workers can no longer afford to live in the city where they work.

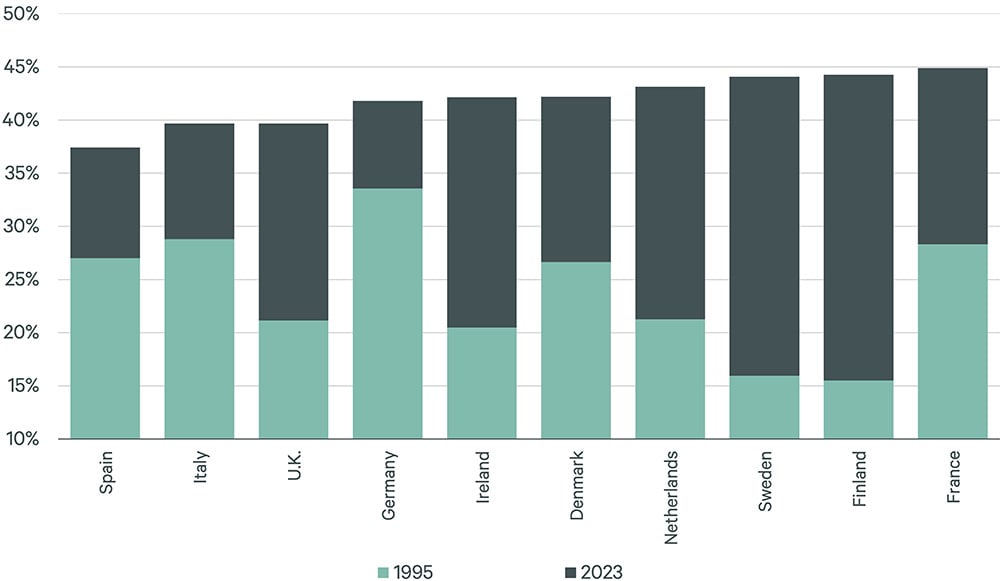

In Europe, the percentage of middle-income earners has grown from 32% of households in 2001 to 42% of households in 2023 and is set to become the largest income group in Europe. This analysis is based on an income threshold of €30k to €70k, as defined by Oxford Economics. However, variances in this income threshold between European cities remain significant. For example, the top threshold for middle-income earners ranges from €50k in markets like Berlin and Rome, to north of €80k in markets like London, Copenhagen and Dublin. Concurrent with the growth in middle-income earners within cities, is an approximate doubling in monthly rents in the top European cities—from approximately €800 per month to €1,600 per month. Over the past two decades, Europe’s rising middle-income earners have become more evenly distributed across the 10 most populous nations, establishing a broad-based demand profile for suitable housing options throughout the Continent.

Figure 1: Proportion of "middle" incomes by country (€30k to €70k per annum)

Despite this demand, affordable options for middle-income earners are limited. The following chart demonstrates a concerning trend—the proportion of middle-income earners paying below market rent is declining, while the share of the same cohort paying market rent or higher is accelerating. Middle-income earners (below the 60th percentile) are the largest group of renters but are increasingly forced to rent on unaffordable open market terms. New housing supply is not being delivered where it is needed most.

Figure 2: Distribution of renters, EU 27* (2007 to 2022)

Note: arrow denotes absolute change in percentage points. Median income is adjusted. Renters paying above and below market rent sum to the total renters by median income.

Source: Eurostat, CBRE Investment Management. For illustrative purposes only.

Europe’s housing structure primarily caters to low incomes, supported by policies focused on raising supply for those with limited means across various housing segments. However, this focus overlooks the much larger—and growing—affordability problem for middle-income earners. The housing shortage for this cohort is prevalent throughout Europe’s largest cities. By splitting out the number of households by income thresholds, we estimate that 57% of households (excluding low incomes below €30k, who will be in social or subsidized housing) are unable to afford the current monthly market rent at 30% of their disposable income, a threshold widely recognized as affordable. This affects approximately three in every five European households, according to our analysis, revealing a stark disconnect between the trajectory of market rents and the underlying housing need. In the U.K., for example, social and public housing, along with rents at subsidized regulated rates, account for approximately two-thirds (65%) of all rental stock. This leaves middle-income earners forced to compete on the open market, where affordability is increasingly out of reach. This skewed housing market structure reveals a compelling opportunity. Investing in affordable housing for the middle-income earners is both a compelling investment diversification and social imperative.

Bridging the Gap

Historical trends and current market dynamics have amplified a long-term middle-income-focused residential investment opportunity. Investors need to understand the landscape to address some of the regulatory risk involved in pan-European residential investing. Perceived regulatory uncertainty surrounding rent control and escalation has tended to draw some investor caution. Throughout Europe, policy is designed to protect tenants, most often achieved through capping or regulating rent increases.

Investors are cautious since they do not control rents as they would in any other real estate asset class. In the residential sector, rent levels and changes in the ability to increase rents can change during ownership which may disrupt business plan execution. In our experience, regulatory intervention to cap rent levels varies widely across European jurisdictions, and even between cities. Periodically, European local authorities introduce short-term focused regulation to keep housing rents affordable, which creates a regulatory risk for investors who require predictable, inflation-linked rent growth. Short-term focused regulatory frameworks that differ between and within jurisdictions adds complexity for investors wanting to make pan-European investment decisions. We believe this issue can be successfully navigated by committing to rent caps linked to inflation. Voluntarily capping rent escalation shields against unpredictable rent control measures and regulatory uncertainty, fostering a more predictable investment environment. It also provides stability in investment returns and aligns with social goals by improving affordability for the forgotten middle-income demographic.

Transparency is a fundamental aspect of this solution, which seeks to balance return expectations with regulatory compliance and tenant affordability. Investors need a clear understanding of the impact of the strategy on investment performance, specifically on the implied trade-off between returns and risk mitigation. While there may be some sacrifice in potential returns compared to the traditional private rented sector (PRS) funds, the strategy discussed above provides the stability and predictability in income streams that are linked to inflation, aligned to core investor requirements. By prioritizing transparency, investors are empowered to make informed decisions that align with their financial and social impact objectives.

Meeting tenants’ rising expectations

Middle-income renters are increasingly seeking housing solutions that go beyond affordability, including features such as wellbeing facilities, sustainability elements, and technology-driven conveniences. For example, utilizing sustainable energy sources in modern residential schemes for middle-income earners align all stakeholder priorities by lowering energy bills for tenants and reducing the carbon footprint for landlords, supporting the environment. The shift in consumer expectations presents a unique opportunity for investors to align with evolving societal demands. Investment strategies that embrace these trends, provide new supply that meets demand where it has evolved to, helping to unwind years of legacy housing that is often no longer fit-for-purpose.

Conclusion

Europe’s forgotten middle has formed a deep and growing demand pool for residential assets across the Continent. This pressing demand presents a compelling, long-term investment opportunity that addresses a growing and often overlooked societal challenge. To capitalize on this opportunity, investors must seek a strategy that navigates regulatory risks across European jurisdictions while aiming to deliver predictable income returns and create positive social impact. This approach aligns with a core and core-plus risk profile, empowering investors to play a pivotal role in closing the affordability gap in Europe’s housing market and fostering a more sustainable future for all.