Market Research

Capturing the Logistics Opportunity in Japan, Australia and South Korea

By: Sandy Padilla, Benedict Lai, Sophie Kao

May 2, 2024 15 Minute Read Time

Several major structural trends are supporting demand for modern logistics real estate across the Asia Pacific region—the continued growth of e-commerce, reconfiguring post-pandemic supply chains, urbanization and sustainability implementation. Many properties in the region require repositioning via conversion, technological investment or upgrading to a higher environmental standard as the current logistics stock ages or becomes obsolete.

From a regional perspective, Japan looks attractive due to several strong structural trends against a backdrop of relatively low interest rates, compared to most other markets. The same growth trends are creating more selective opportunities in Australia and South Korea, where we also see the potential for tactical transactions.

For Australia and South Korea, we believe the coming years may also offer historically advantageous entry points into private real estate while asset prices adjust as inflation and interest rates moderate from high levels. Committing capital at this stage of the repricing cycle can provide the opportunity to capture bottoming prices in private real estate, which can yield strong vintage returns.

Macro environment remains supportive

Economic growth and demographic trends vary by country but, in aggregate, support logistics growth across the region. The Asia Pacific region continues to show resilience, even after the challenges of 2023, including elevated inflation, high policy rates (except Japan), banking solvency concerns and a weaker-than-expected Chinese reopening rebound. The region is well-positioned for a recovery in 2024—inflation is expected to continue easing and the tightening cycle will likely conclude in many markets, leading to more pricing clarity.

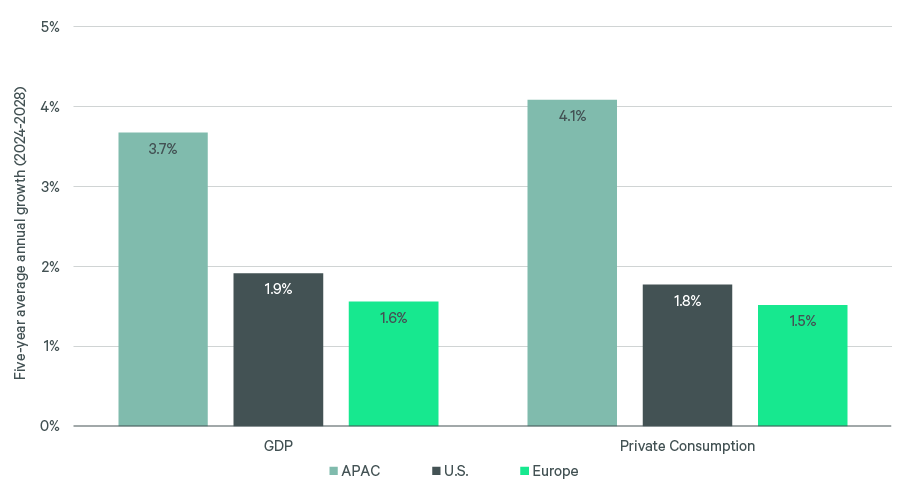

Asia Pacific economic growth is expected to moderate to 3.8% in 2024, down from 4.2% in 2023, according to Consensus Economics, but will remain comparatively strong. Over the next five years (2024-2028), growth in the region is forecast to average 3.7% annually, compared to 1.9% for the U.S. and 1.6% for Europe, according to Oxford Economics (Figure 1).

Figure 1: GDP and private consumption, five-year average annual growth (2024-2028)

We expect private consumption growth to average 4.1% annually over the next five years (2024-2028) in Asia Pacific, compared with 1.8% for the U.S. and 1.5% for Europe. Due to an urbanization trend, the populations in several major cities, including Tokyo, Osaka, Fukuoka, Singapore, Melbourne and Sydney, are forecast to grow over the next five years—despite population declines in some countries, including Japan. We expect occupier demand in the logistics sector to be supported by this population growth, combined with lower logistics space per capita across many major cities in the Asia Pacific region, especially compared to the U.S. and Europe (Figure 2).

Figure 2: Modern logistics space per capita in major metro areas across APAC, the U.S. and Europe

Even in Seoul, where the population is forecast to decline by 3.3% cumulatively over the next five years, online retail sales are expected to remain robust and support logistics demand, given that South Korea is the fourth largest e-commerce market globally (by 2023 e-commerce sales, according to Euromonitor).

Demand drivers for Asia Pacific logistics are strong

In Q4 2023, aggregate Asia Pacific logistics rents continued to grow, increasing by 0.6% quarter-over-quarter (Q-o-Q) and 4.6% year-over-year (Y-o-Y), according to CBRE. Three key drivers of long-term demand and pricing remain in place.

E-commerce: Internet retail sales continue to drive demand for Asia Pacific logistics. China, South Korea and Japan are three of the five largest e-commerce markets globally for online retail sales, according to Euromonitor. Although e-commerce growth is moderating in some markets, the share of e-commerce sales to total retail sales remains elevated compared to pre-pandemic levels. CBRE Research projects that for every US$1 billion of additional e-commerce sales, an additional 1 million square feet (92,903 square meters) of logistics space is required.

Undersupply of modern logistics stock: Many Asian cities have a structural undersupply of modern logistics facilities. Logistics space per capita ratios in many Asian cities are much lower, compared to more established U.S. logistics markets. Looking ahead, occupier interest in modern logistics facilities is expected to continue, given increased demand from e-commerce retailers and a continued shift from “just in time” to “just in case” supply chain logistics. New technologies require next-generation facilities that provide key building features, such as higher clear heights, stronger floor foundations, high-capacity roof loads, efficient column spacing, larger truck courts and enhanced power.

Reconfiguring supply chains and reshoring manufacturing: Following supply chain disruptions during the pandemic, companies in many markets have been focused on increasing supply chain resilience. Strengthening and diversifying supply chains includes reshoring manufacturing, which is most evident in Japan. The global semiconductor production race is also creating the need for substantial supply chain expansion, fueling logistics demand across all parts of the supply chain, from raw material suppliers to packaging and testing companies.

Identifying opportunities in Japan

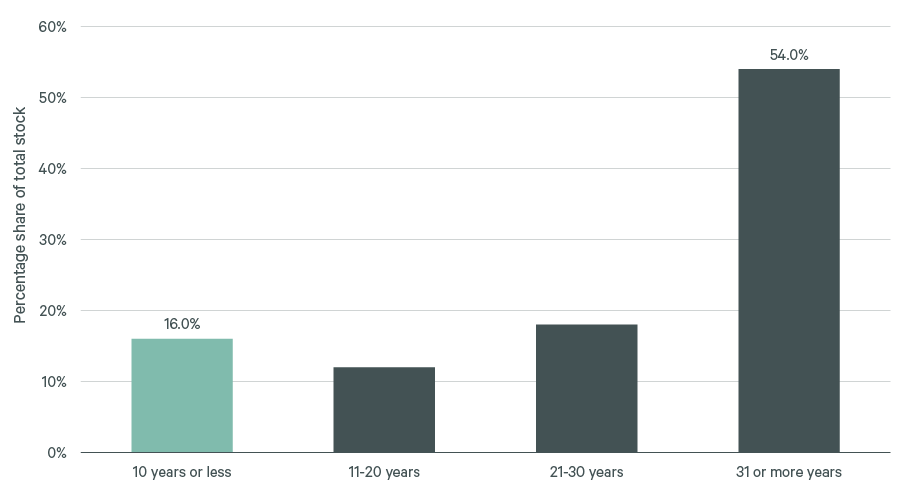

Currently, Japan offers some of the best opportunities in Asia, for a wide variety of reasons, starting with structural undersupply of modern logistics facilities. The majority of Japan’s logistics facilities are outdated—54% are more than 30 years old and only 16% were constructed within the last 10 years (Figure 3).

Figure 3: Japan’s warehouse stock by age

A good example of Japan’s need to modernize warehouses is in the cold storage subsector, which is increasingly attractive due to low vacancy and the lack of suitable sites that can support growing frozen food consumption in Japan. As maintenance costs increase year-over-year, and performance in energy efficiency deteriorates, cold storage facilities are more prone to obsolescence than ordinary warehouses. In addition, hydrochlorofluorocarbon (HCFC) restrictions will require some assets to be redeveloped over the mid- to long-term to meet new sustainability standards.

Japan’s structural undersupply is being further pressured by such factors as e-commerce growth, the reshoring of manufacturing, a change in truck-driving regulation and accretive financing.

According to CBRE Japan research, manufacturing inventory is set to emerge as the next driver of logistics demand, alongside 3PL and e-commerce growth, particularly in Greater Nagoya (for automobiles) and Greater Fukuoka (for semiconductors). In Japan, raw materials inventory has grown by 60% during the Q4 2019–Q4 2023 period. Information and communications electronics equipment manufacturing raw materials inventory grew 92%, while automobile manufacturing raw materials inventory grew 105% over the same period, according to the Japanese Ministry of Finance.

The “2024 problem,” where changing regulations will limit truck driver working hours starting in April 2024, is expected to create additional demand for logistics facilities. Truck drivers are already in short supply and logistics operators will likely need new locations in between large cities.

Financing still looks attractive in Japan. Japan’s interest rate is the lowest in the region and expected to remain so, despite monetary policy normalization. Japan offers positive and wide spreads between logistics cap rates and lending costs (Figure 4).

Figure 4: Spreads between logistics yields and lending rates across select major metro areas

Looking ahead, the Japanese logistics supply pipeline is forecast to moderate, as increased construction costs restrain some development. Supply pipelines have increased in certain markets. Submarket selection and the ability to offer points of differentiation in building quality and occupier service will be crucial.

Narrowing in on Australia and South Korea

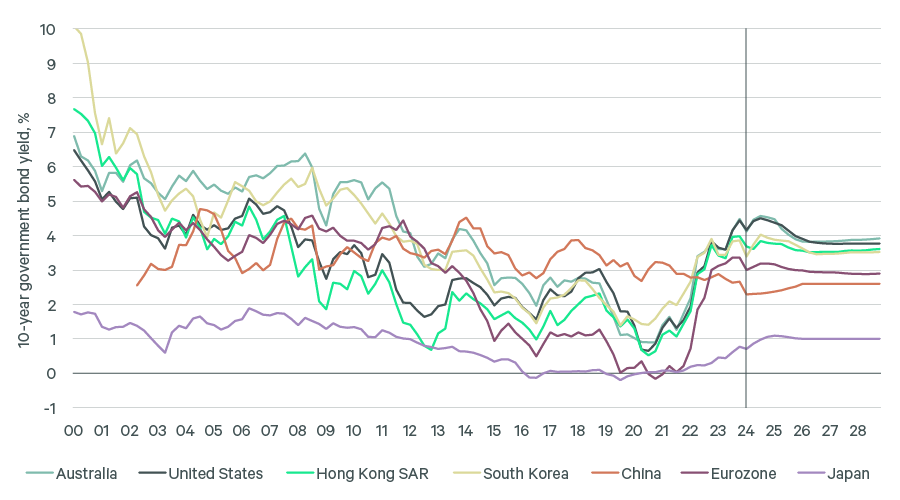

In contrast to Japan, most developed markets, including Australia and South Korea, are likely to begin cutting interest rates in early 2025. As a result, bond yields in Australia and South Korea are forecast to decline (Figure 5).

Figure 5: 10-year government bond yields since 2000 (forecast starting Q2 2024)

Repricing is already underway in both Australia and South Korea, which were the first two developed Asia Pacific markets to raise interest rates and are also likely to be the first to start cutting rates. Construction firms that have been under pressure from recent high financing and construction costs could benefit from potential recapitalizing opportunities once rates decline.

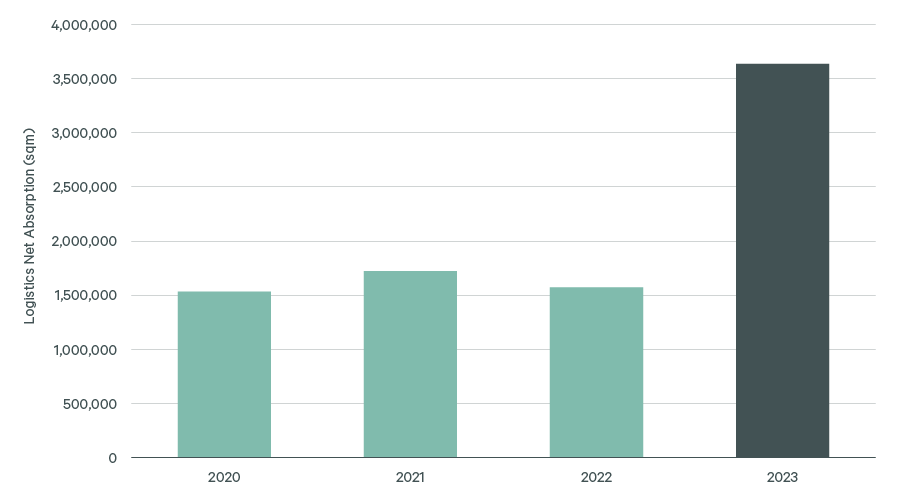

In South Korea, fundamentals supporting the Greater Seoul logistics market remain intact despite some near-term headwinds. In 2023, Greater Seoul logistics absorption was a record 3.6 million sqm, 126% higher than the 1.6 million sqm annual average during the pandemic (2020-2022) (Figure 6). This record absorption in 2023 was primarily driven by 3PLs and e-commerce, according to CBRE.

Figure 6: Greater Seoul logistics net absorption (sqm)

However, South Korea’s warehouse sector is working through a period of overbuilding, especially in the cold storage subsector. This marked contrast to Japan reinforces the need to fully understand submarkets in each country.

Given robust demand in 2023, the Greater Seoul overall vacancy rate began to decline in H2 2023 but remains elevated compared to the pandemic period (2020-2022). Certain submarkets and logistics types are more resilient than others and high-quality logistics stock per capita is considerably lower relative to other developed global markets. The supply situation is expected to stabilize beyond 2024 due to higher construction costs.

In Australia, growing e-commerce sales and the need for faster, more efficient delivery of packages has led to increased tenant demand for metropolitan industrial sites—vacancies are less than 2% in Sydney, Melbourne and Brisbane as of H2 2023. Australia’s e-commerce sector is less established than other developed economies and will continue to catch up as the presence of e-commerce drivers in this market increases. Over the next four years, 1.1 million sqm of additional e-commerce dedicated logistics space will be required in Australia to support the growth of internet sales, according to CBRE. Australia’s strong long-term population growth should also support logistics real estate.

Investing in a potentially attractive vintage

We believe this stage of the real estate cycle will create an attractive vintage of opportunities in Australia and South Korea. Following a significant contraction in debt and equity capital availability in South Korea, asset values in the public market have quickly repriced; private market valuations are now starting to adjust.

Japan looks attractive due to several strong structural trends against a backdrop of relatively low interest rates, compared to most other markets.

We remain committed to the Asia Pacific logistics sector. Long-term underlying trends such as e-commerce, supply chain reconfiguration and rising incomes still favor logistics investments in the region. A deep understanding of local market conditions and dynamics is critical to seek to position our investments for future outperformance. We expect to see a bifurcation in performance with higher-quality modern logistics assets in supply-constrained submarkets best positioned for the future.