Investment Perspectives

Listed Real Estate: A solution for modern portfolios

August 4, 2024 5 Minute Read Time

Author

Senior Director, Portfolio Strategist

Download the Full Report

View Summary Video

We see listed real estate as both a strategic allocation for investors and a compelling opportunity when considering the current real estate cycle. When we review, we find listed REITs can provide:

A portfolio enhancement and complement:

- REITs have provided superior returns over the long-term; a compelling portion of return is driven by attractive and growing income.

- REITs can provide diversification; their inclusion into an equity/bond portfolio has improved total returns without unduly increasing risk.

- REITs can complement private real estate by improving risk-adjusted returns, augmenting sector exposures and providing liquidity essential for dynamic real estate management.

An opportunity in today’s markets:

- Following a historic pace of global central bank rate hikes, listed valuations have disconnected relative to equities and private real estate markets; we see a potential cycle of above-average returns ahead.

Keys to outperformance from active management:

- As a niche asset class, listed real estate offers advantages to specialized active managers, who can outperform benchmarks over time and enhance returns for investors.

The Real Estate Opportunity

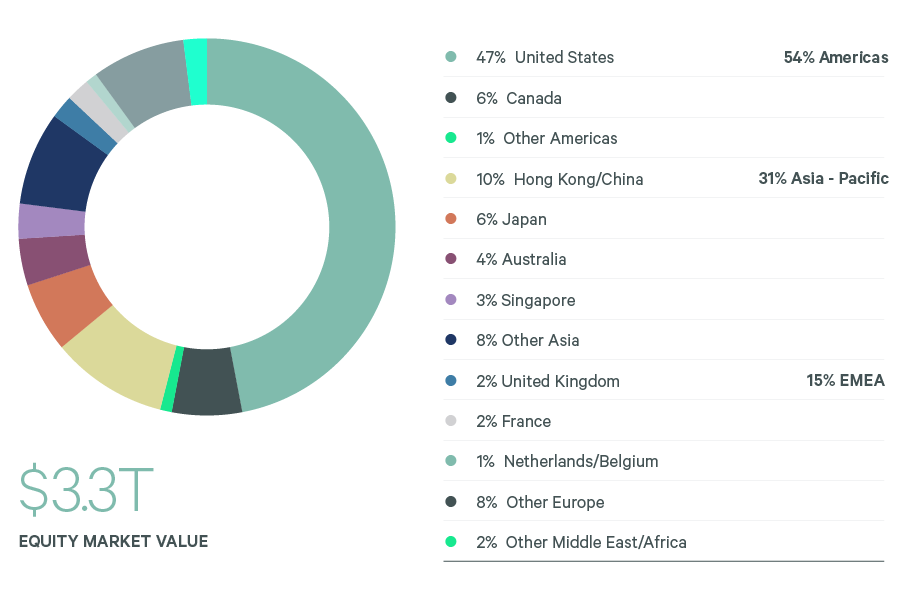

Globally, the real estate market represents a $41 trillion opportunity, with listed real estate comprising over $3 trillion in market cap.1 Institutionally, $1.7 trillion of capital sits with global real estate managers, with listed real estate comprising ~$300bn.2 Listed real estate touches nearly every facet of modern life. The majority of REITs focus on different property types, with different drivers affecting rent collection; they also tend to have different durations for contracts. As a result, REITs offer an attractive combination of resiliency and economic exposure in a comprehensive and liquid investment universe.

The global listed real estate universe

Example Sectors

A Portfolio Enhancement and a Complement:

Competitive long-term returns

REITs have provided superior returns over the long-term. A compelling portion of total return is driven by growing income that offers the opportunity for inflation protection.

Over the last 25 years, listed U.S. real estate generated returns of ~9% and global real estate ~7%. This includes the headwinds of weaker performance over the last five years, which saw both the impacts of the COVID 19 pandemic as well as that of a historic rate hiking cycle. (During the last five years, global listed real estate delivered approximately a flat return). In part because of this recent lag, we believe listed real estate returns today have the potential to eclipse the long-term track record, in which REITs have led other asset classes and provided competitive Sharpe ratios.

REITs have led total returns and provided competitive risk adjusted returns

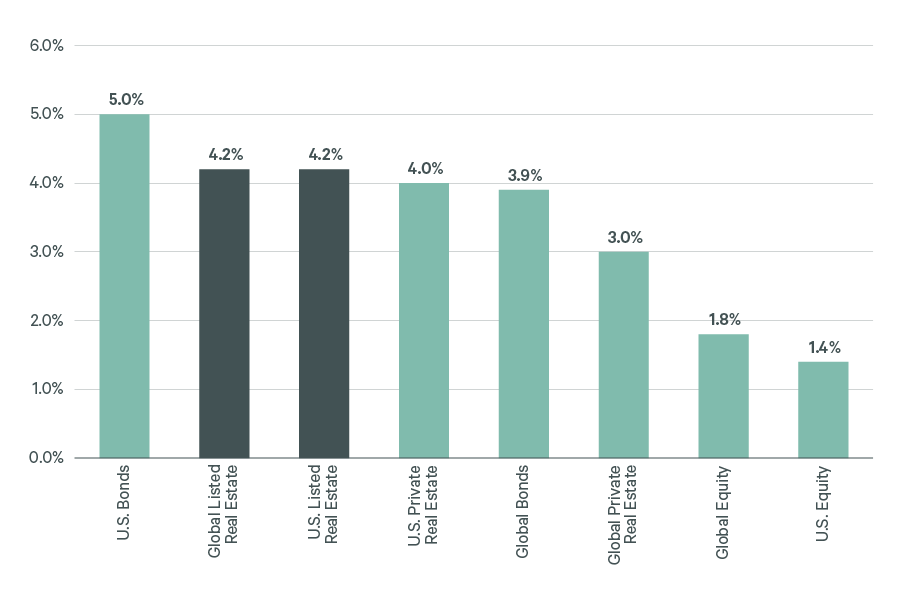

Attractive and growing income

REIT income has historically constituted over half of total returns. As of June 2024, current REIT dividend yields stood above 4%. Dividends are likely to grow at a mid-single rate or better over the next several years.

When considering alternatives, REIT yields are competitive against broad equities and private real estate. They are attractive compared to bonds when further considering their potential for income growth and the capital appreciation potential they can offer.

REIT dividend yields compared to alternative income sources

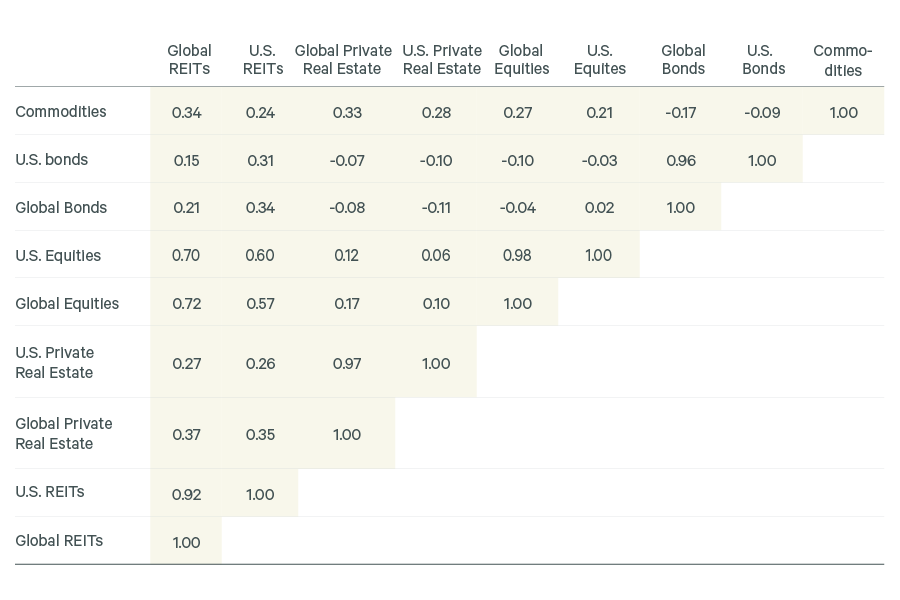

A diversification benefit

Inclusion of REITs into a traditional portfolio can provide a diversification benefit since the asset class has low correlations to other assets. While REITs have correlated with bonds more recently—during the hiking cycle of 2022 and 2023—this has been an aberration to the long-term trend. Growing dividends and businesses that benefit during inflationary periods have contributed to listed REIT performance over time. Later in this paper, we discuss the correlations of listed and private real estate when adjusting for the lag effect of private real estate valuations.

REIT asset class correlations over the long-term

Enhancing returns and blending REITs

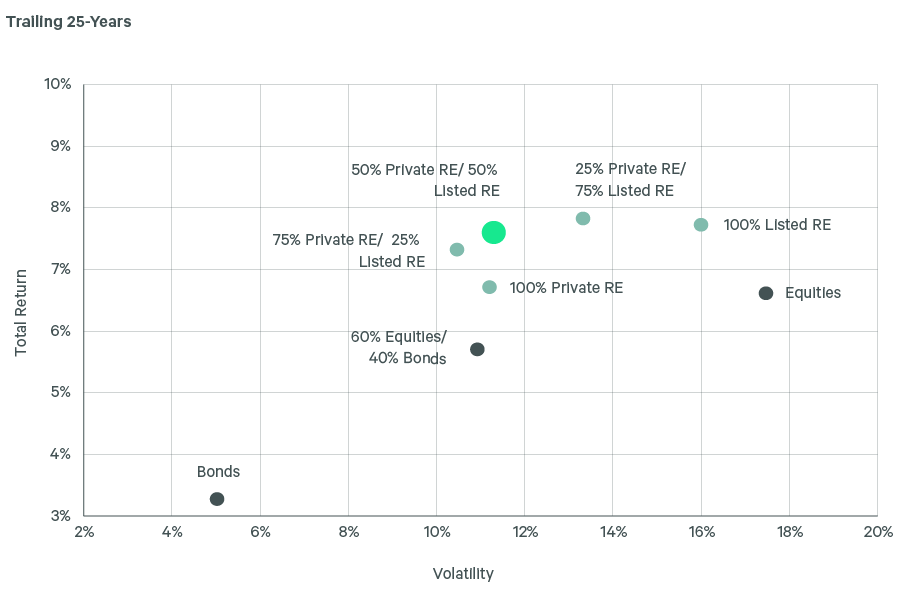

The inclusion of listed real estate with a traditional equity/bond portfolio has improved total returns without unduly increasing risk. Our data below includes the headwinds of the last five years (COVID 19 and the global central bank rate cycle). During this time, global listed real estate lagged global equities by ~12% on an annualized basis. We see an enhanced opportunity for listed real estate when looking ahead.

Blending listed real estate has enhanced total returns over the long-term

Listed as a complement to private real estate

Over 64% of the world’s largest real estate investors invest in REITs. They do so for several reasons. Within a real estate allocation, listed real estate can improve risk adjusted returns. Listed property, which often leads private by approximately three quarters, can capitalize on mispricing while providing outsized exposure to next generation real estate exposures. Listed can also provide the liquidity that offers the potential for dynamic management of real estate over the course of a cycle.

Among CBRE IM clients, we have seen an acceleration in the use of hybrid portfolios of real estate with both listed and private allocations. We provide a summary of our findings below:

Considering hybrid real estate portfolios

Listed has improved risk adjusted returns over the long-term

Listed and private real estate are aligned; listed tends to lead private returns by approximately three quarters.

Listed offers next generation property, including data centers, cell towers, net lease, healthcare, single-family rental and other assets under-represented in private markets. Office comprises only three percent of the listed universe.

Listed offers the opportunity to capitalize on mispricing and the liquidity needed for dynamic management.

An Opportunity in Today’s Markets

We believe a new cycle for listed real estate began in the fourth quarter of 2023, following nearly two years of negative asset-class returns, with the recognition of a potential pause in global central bank interest rate hikes.

Today’s starting point for listed real estate is favorable. At the end of Q2 2024, global real estate sits at a double-digit discount to our assessment of net asset values, with implied cap rates at a spread of several hundred basis points from private market appraised values. Compared to broad equities, REITs sit at an approximate 20% discount on a forward multiple, compared to a history of a roughly on par valuation. Whether from private markets, if liquidity is available, or from broad equities, we see an opportunity to de-risk holdings and add to those in listed real estate.

We believe REITs have the potential to deliver a robust annualized return, powered by a mid-single digit current dividend yield, mid-single digit annualized earnings growth, modest multiple expansion, and the potential for active management. Recently, some of CBRE Investment Management’s largest listed REIT institutional investors have increased their REIT holdings; we expect that allocations will continue from a variety of investors.

The REIT Return Proposition

The Advantage of Active Management

For investors, active REIT managers can deliver enhanced returns from a niche asset class that provides keys to durable alpha. REITs are linked to a vast private market, where integrated managers can possess an information edge. REITs are often under-followed by generalist equity analysts, benefitting those with specialized coverage. With diverse businesses and contract terms, different REITs can provide varying performance over the course of a cycle—aiding managers with a rigorous sector allocation process.

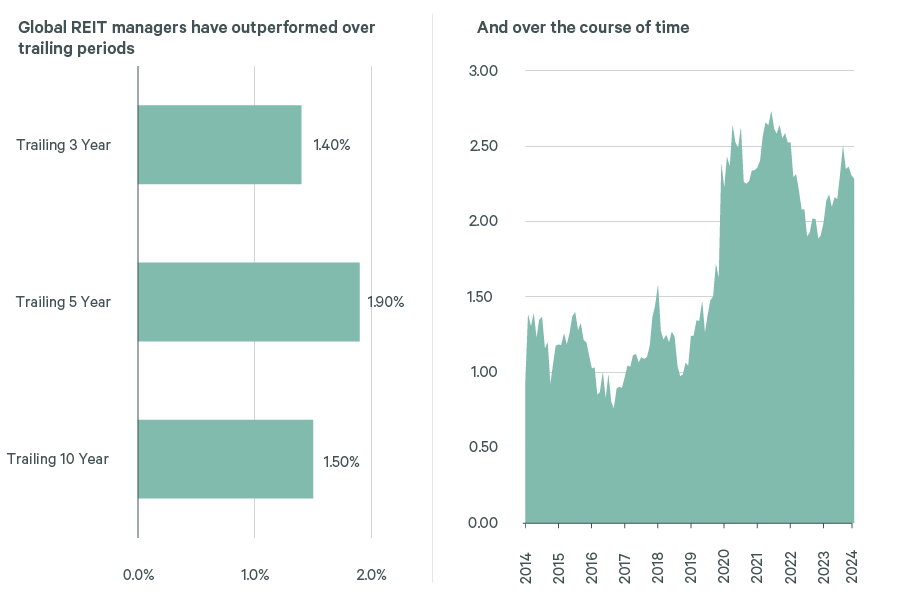

When we review the performance data, REIT managers are who the scoreboard says they are. Over extended time frames, REIT managers in general have outperformed their benchmarks. Further, this alpha has been strong over time; in the bottom left, we show trailing outperformance, while in the bottom right we show rolling five-year alpha over the last decade—this has ranged between approximately 80-270bps, which is comfortably above typical management fees.

Notably, REIT manager rolling outperformance strengthened during the COVID-19 pandemic, which is reasonable considering that active managers often find opportunity in dispersion during distressed markets. As investment cycles have become more compressed in recent years, with the potential for higher dispersion, we expect greater opportunities for active management when looking ahead.

The REIT Manager Scoreboard

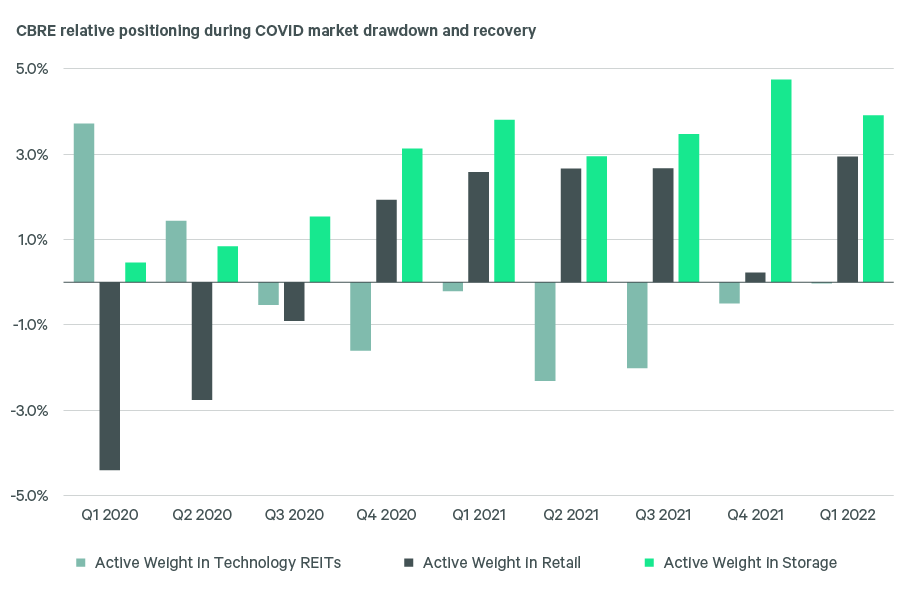

COVID 19 provided an excellent example of CBRE Investment Management’s listed investment process in action. As COVID 19 spread in early Q1 2020, the digital real estate and industrial sectors (which are relatively resilient) outperformed listed benchmarks by ~35% and ~17% while malls (which largely closed) declined and lagged by ~28%. With dispersion across sectors and individual companies, our strategies repositioned for a new normal in U.S. office. We focused on security selection within apartments, single-family rental, and life science to relatively outperform during this time. Given our integrated market advantage, our portfolio managers identified opportunities between public and private assets to optimize holdings relative to net asset value and benefited from the recognition of that value in the market.

As summer progressed, our strategies rotated away from the digital real estate sector, which our tools flagged as relatively expensive. At that time, our team bought discounted mall and storage assets. Our analysis, which included a review of rent trends and tenancy health, led to sizable active selections within these sectors, which led to outperformance in Q2 2020. In Q3 and Q4 of 2020, we added to high conviction holdings within the mall space and storage sector. Based on research from the broader CBRE platform, channel checks, and analyst modelling, we saw storage as a sector with potentially double-digit revisions to estimates and NAVs. By the end of 2020, we had made storage a significant active weight for our portfolios.

Collectively, our decisions paid off with outperformance for investors during this period—both stock selection and sector allocation contributed to our strong relative returns.

An Essential Asset Class for Today’s Investors

We see listed real estate as both a strategic allocation for investors and a compelling total return potential when considering the current cycle. Listed real estate can both complement and enhance traditional and private equity portfolios. It provides improvements to potential total return, income contribution, property sector exposures, and investor liquidity.

When considering our outlook, listed real estate offers both compelling current dividend income, as well as significant capital appreciation potential. We believe this positive total return outlook will be enhanced by active management. We are excited by the opportunity to deliver for investors as this new cycle for listed real estate outperformance unfolds.

1 Global commercial real estate market opportunity per CBRE Investment Management and Oxford Economics forecasts as of June 30, 2024.

2 Source: Assets under management per Preqin and CBRE Investment Management as of December 31, 2023. Listed AUM represents eVestment and Morningstar Direct as of December 31, 2023, including institutional separate accounts and funds. Data excludes closed-end funds and Japan domiciled open-end funds.