Market Research

A new outlook for European residential real estate

November 18, 2024 5 Minute Read Time

Author

Director – Insights & Intelligence

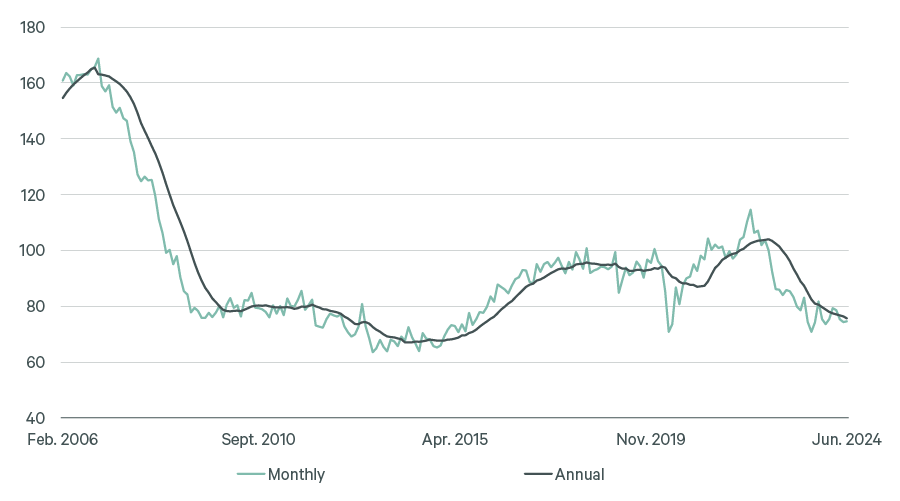

After a challenging two years for all real estate markets, the evidence now clearly shows Europe is at a turning point. The residential sector, in our view, should lead the recovery heading into the next cycle, with capital values returning to growth in Q2 2024 for the first time in seven quarters. Attractive occupational fundamentals, healthy income growth potential, and increasing signs of capital values having bottomed out, now provide a compelling window of opportunity for investors to deploy capital in this sector.

Figure 1: European MSCI capital values, Q2 2022-Q2 2024, % Q-o-Q and cumulative

This note outlines our latest house view for the sector and why we think residential has shifted gears to become a core mainstream allocation in European real estate portfolios.

Tide of investor sentiment is turning

Residential investment activity in 2023 dropped around 60% from its peak. While 2024 is unlikely to see a surge in recorded deal flow, the broader improvement in investor sentiment should provide the platform for a steady recovery heading into 2025. Prime residential yields have moved out between 100-150bps on average over the last two years, with transaction yields in major European cities now between 3.5% to 4.5% on a net initial basis. The latest evidence suggests yields are now stabilizing, with bid/ask spreads narrowing over the last few quarters.

While debt costs are still only accretive in select markets such as Germany and Denmark, our expectation is for improvements over the next 12-18 months as the ECB progresses with additional rate cuts. This should drive a prudent increase in leverage as the transaction market recovers.

With many investors still underweight to residential versus target allocations and wanting to gain scale quickly, these factors provide the green light that many have been waiting for. Prior to the inflation shock, residential had grown to around 20% of market investment activity. We expect the sector to gain increasing share over the medium- to long-term.

Healthy income growth potential but tenants increasingly discerning

Open market rental growth has moderated from the highs of the last two years but should still trend above inflation as supply constraints continue to grow. Higher build and financing costs, alongside pockets of regulatory uncertainty, have created material headwinds in the construction sector, with new housing permits falling 27% since their post-COVID peak. Across Europe, residential permits are now in line with the record lows following the Global Financial Crisis and should continue to bolster healthy real estate income growth in the sector.

Figure 2: EU-27 residential build permit index, 100=2021

Investors need to stay disciplined when pricing rents to match local earnings. Letting success and occupancy are highly correlated with aligning the rent level and amenities with each submarket and local demographic. Even in residential, where vacancy rates typically sit below 2% in major European cities, tenants are often looking for long-term homes with inclusive social communities. They come with a long list of requirements to satisfy before committing to a lease. Getting this right is critical in ensuring deep and happy tenant pools and driving long-term sustainable cash flow.

Return outlook now close to cycle peak, offering strong investor value

Rebased entry yields and the robust occupational outlook have driven a steady upgrade in our total return outlook for the last few quarters. The latest return number of 7.7% per annum for Europe overall is likely now close to the cycle peak, offering a compelling entry point for new equity. With residential yields expected to gradually trend inwards again from 2025-2026, this should further support the upside potential for capital values.

By comparing this return outlook with the sector’s calculated required return, our Risk Adjusted Real Estate (RARE) tool assesses whether an investor is being adequately compensated for the risk they are taking. With European residential now screening well, both relative to all property and on an absolute basis, our model suggests it’s an excellent time to be deploying capital.

Figure 3: Required return & total return for residential markets (24Q4-29Q3)

Stand out markets include Germany and the U.K., while cities such as Amsterdam, Madrid, Stockholm and Copenhagen also offer attractive value. Not all residential markets in Europe are expected to perform as strongly. Regulatory factors have held back both Barcelona and Dublin and higher supply levels in Helsinki have curbed our rental outlook there.

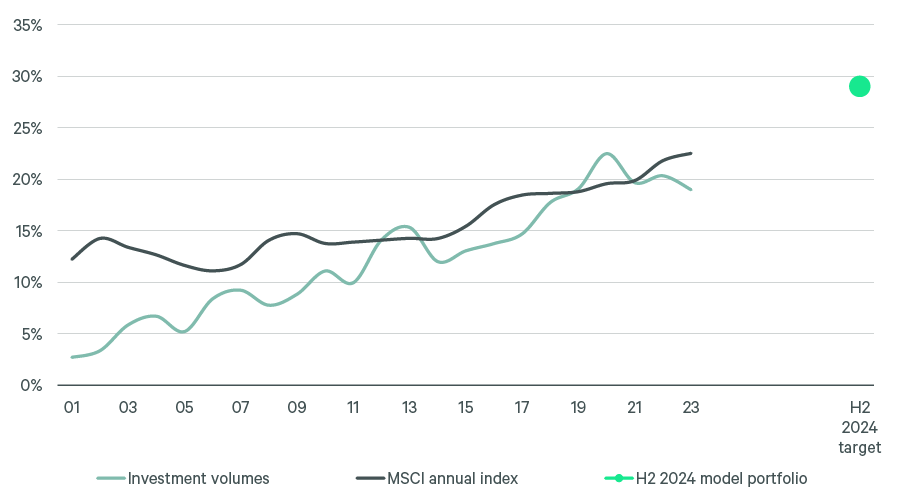

Residential is the largest overweight in our model portfolio

Our model portfolio for Europe is informed by both our return forecasts and RARE analysis and illustrates our portfolio allocation preferences. The tactical allocations vary with each new set of forecasts and RARE analysis to reflect current recommendations.

Residential remains one of our top conviction model portfolio allocations at 29%, and holds by far the largest overweight position relative to the benchmark. There has been a clear direction of travel for European residential allocations over the last decade with the sector moving out of the alternative bucket to become a core mainstream allocation.

Figure 4: European residential as % of all property

Investors in residential have become increasingly sophisticated in their approach, either via targeted strategies, more nuanced underwriting or learning lessons from recent periods of economic shock. As investors have scaled up, gained track record and built out operational expertise and platforms, there is now a better understanding of how to deliver and manage a successful build-to-rent (BTR) product. In our view, residential allocations will continue to see a structural shift driven by an increasingly institutionalized investment universe taking market share from the private rental market.

Affordable housing offers optimal risk-adjusted performance

Affordability concerns are now one of the largest constraints on future rents with the evolving regulatory landscape high on the agenda in most local markets. For the most part, regulation in Europe remains relatively predictable, forming a hurdle which can be priced in, rather than a barrier to entry. Regulation typically offers investors a stable, more consistent cash flow. Pending or sudden changes to rent regulation often create investment uncertainty, and can have a tangible impact on market performance if not prudently underwritten. Investing in housing which is affordable to everyday users, with a greater focus on achieving long-term sustainable rent growth, rather than chasing short term gains, should help to mitigate the risks of future regulatory change. More affordable housing has proven to generate higher occupancy levels, larger demand pools and lower rent volatility through market cycles, driving improved risk-adjusted performance.